Stock Markets

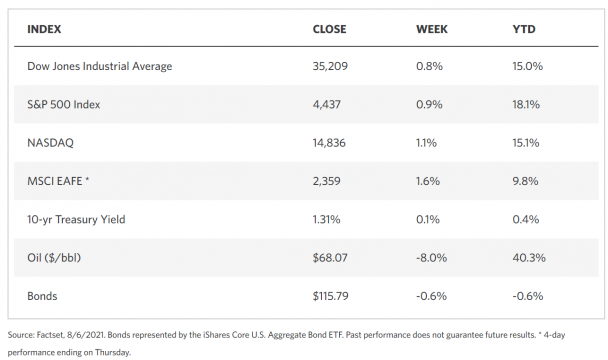

Equities charted gains for the past week as the large-cap benchmarks and tech-heavy Nasdaq Composite Index surged to record highs. A steep increase in the longer-term interest rates after the strong monthly payrolls report last Friday bodes well for the lending margins of banks, thus propping up the financial sector. Also moving up are the prices of small utilities stocks, although the energy sector underperformed in the S&P 500 Index. Trading slumped at the start of the week, possibly due to worries of the delta variant and discounting of earnings reports. Business segments that are central to the reopening of the global economy – airlines and travel, entertainment companies, big retailers, cosmetics companies, payment processors, and industrial metal manufacturers – showed particular weakness. Sentiments were also weighed down by China’s enhanced regulatory measures. The latter days saw the market energized by some unexpected earnings reports, with second-quarter earnings for the S&P 500 counters possibly increasing by over 85% year-on-year.

U.S. Economy

The closely watched monthly payrolls report issued by the Labor Department gave reason for optimism as the payrolls grew more than consensus expectations. There were 943,000 new jobs added in June, the effect of easing of lockdowns in the summer of 2020. April and May’s increases underwent an upward adjustment; the labor participation rate and average weekly hours rose, and the average hourly earnings growth (4%) increased higher than initially forecasted (3.8%). The unemployment rate fell to 5.4%, its lowest since the pandemic. Overall, the jobs report was reflective of the fundamentally favorable underlying economy.

- In the first two quarters of 2021, GDP growth averaged 6.4%, buoyed by a significant improvement in the labor market. The optimistic jobs report released during the week fuels optimism in the build-up of economic momentum and that it will be sustained for the rest of the year as a result of a recovering employment situation. The possibility of increasing inflation pressures should not be surprising as a result of fast-rising wages, which may prompt concerns about implications for Federal stimulus. The likelihood of policy changes may be tempered by the delta variant’s impact on the reopening of the economy and its possible effect on the pace of GDP growth.

- It is unlikely that the delta variant will derail the wider expansion of the economy even if its pace of growth may be disrupted. The projected GDP growth for the year remains between 6% and 7% and may experience a slightly slower (but still above-trend) growth rate for next year. As a result, corporate earnings growth can be expected to have a resilient foundation and drive the market moving forward. More than 80% of the S&P 500 have already reported second-quarter earnings for this year, registering 101% higher on a year-on-year basis. The 2021 S&P 500 earnings are forecasted to exceed their pre-pandemic level by 31%, and presently the index is already higher by 30% compared to the 2019 year-end level. This indicates that equities continue to remain linked to the economic fundamentals. It is therefore plausible that and volatility linked to the pandemic or tapering may be seen as opportunities for portfolio-rebalancing.

Metals and Mining

During the past week, the gold spot price descended by 2.82%, closing at $1,763.03 per ounce from the earlier week’s close of $1,814.19. Earlier in the week, the metal ticked upwards to $1,816.08 as a result of U.S. 10-year Treasury yields falling to a neat two-week low and the dollar index correcting 0.1% against its rivals. Since the price of gold has a resistance level at $1,830, its recent strength appears to have triggered some profit-taking and prompting the subsequent fall in price. Towards the end of the week, however, gold’s price broke down significantly due to trading off-balance when U.S. Treasury yields suddenly surged higher from their previous lows. The 10-year yields jumped 7 basis points within one hour after the Fed Vice Chair announced that a 2023 rate hike is consistent with the central bank’s new framework. Gold investors, who were then buying up the metal on risk-off trades, were whipsawed as sovereign yields sent bond prices heading sharply upwards. The gold sell-off was investors’ reaction to the aversion to shouldering the opportunity cost of holding gold when interest-bearing instruments are moving higher.

The price of other precious metals followed the direction of gold’s descent. Silver’s drop exceeded by proportion that of gold, losing 4.55% of its value when it closed at $24.33 per ounce from the previous week’s close of $25.49. Platinum descended even further, dropping 6.46% from last week’s close of $1,051.55 to Friday’s close of $983.58 per ounce. Palladium also gave up 1.28%, the least price drop by proportion, ending at $2,628.80 from the previous week’s close of $2.662.94 per ounce. Base metals also absorbed some contagion from the trend in precious metals. Copper lost 2.67%, dropping from $9,728.00 to $9,468.00 per tonne. Zinc gave up 1.44%, sliding from $3.027.00 to $2.983.50 per tonne for the week. Aluminum lost marginally by 0.46%, dipping to $2.578.00 from $2,590.00 per tonne. Tin bucked the trend, however, rising 0.29% from $34,649.00 to $34.750.00 per tonne.

Energy and Oil

Oil price recovered somewhat on Friday from the week’s collective decline; that being said, caution still dominates in the oil markets, mindful that China and the U.S., its two largest players, are still contending with the covid surges. Another component of the oil market’s geopolitical risk is added by tensions in the Persian Gulf, it was however offset by the hike in U.S. crude inventories during the week.

The future demand for fossil fuels appears to be further compromised by the plans put forward by Biden’s White House calling for half of cars and trucks in the U.S. to be comprised of electric vehicles (EV), plug-in hybrid electric vehicles (PHEV), or fuel cell vehicles by the end of the decade. The non-binding executive order notwithstanding, policies appear to be more aggressively headed towards greater fuel economy standards than they were previously. In the meantime, hopes for a more diplomacy-focused Biden administration to ease sanctions are prompting negotiations between the Venezuelan opposition and the Maduro-led government. Meanwhile, in another part of the world, Russia is contemplating a three-month ban export ban on gasoline. This is in reaction to the two-pronged dilemma of increasing domestic demand and lower refinery production due to prolonged maintenance.

Natural Gas

The price of liquefied natural gas (LNG) ascended in Asia to an 8-week high as a result of higher-than-average temperatures driving greater demand for air-conditioning power. In Asia, spot LNG prices for the September delivery date rose to almost $17 per million British thermal units (MMBtu), amounting to nearly a $1.50/MMBtu increase from last week. In most locations for the recent report week (July 28 to August 4), natural gas spot prices climbed. The Henry Hub spot price went up from $4.05/MMBtu at the start of the week to $4.12/MMBtu at the week’s end. The August 2021 New York Mercantile Exchange (NYMEX) contract expired on August 4 at $4.044/MMBtu. The September 2021 NYMEX contract price rose to $4.158/MMBtu, an increase of $0.12/MMBtu week-on-week. The price of the 12-month strip averaging September 2021 through August 2022 futures contracts ascended by $0.10/MMBtu to $3.854/MMBtu.

World Markets

In Europe, equities surged due to strong corporate earnings growth and renewed prospects of a recovering economy. The pan-European STOXX Europe 600 Index closed 1.78% higher than the foregoing week. Major stock indexes also outperformed, with Germany’s Xetra DAX Index gaining 1.45%, Italy’s FTSE MIB Index rising 2.51%, and France’s CAC 40 Index advancing 3.09%. Likewise rising by 1.29% is UK’s FTSE 100 Index. The core eurozone bond yields have moved lower in reaction to the possible increase in coronavirus cases hampering the further enhancement of the continent’s recovery. Peripheral eurozone bond yields followed the core markets’ trend for the most part. The UK gilt yields slid in conjunction with the core markets. The correction in yields was subsequently moderated in response to hawkish pronouncements by the Bank of England (BoE) that modest tightening of monetary policy is still possible. The outlook, however, is for the economy to continue to grow 7.25% this year, and for the GDP to increase next year by 6% rather than the previously forecasted 5.75%.

Japan’s stock markets overperformed in the past week. The Nikkei 225 rose 1.97% while the broader TOPIX Index climbed 1.49%, driven by the listed firms’ positive earnings reports. The optimism was somewhat dampened by the rise in coronavirus cases in the country, topping 5,000 for the first time. An advisory panel of experts cautioned the country may face a further deterioration of the situation. Cases across the nation already reached the highest level on record, prompting the government to expand its quasi-state of emergency to eight additional prefectures where the highly contagious delta variant is expected to be spreading. Based on this outlook, the yen remained unchanged, ending the week at JPY 109.7 to the USD. The yield on the 10-year Japanese government bond dropped modestly to 0.01%.

In China, stocks climbed to recover some of the ground lost in the previous week’s sharp declines. Buyers went bargain hunting, pulling the Shanghai Composite Index up by 1.8% and the large-cap CSI 300 Index by 2.3%. Domestic investors were still careful to sidestep market sectors that came under the watchful eye of the government and instead went for stocks that enjoyed strong official support. Negative comments by the state media regarding online gaming dampened investor sentiment, giving the impression that the industry may come under tighter government regulation. Following positive profit alerts and share buyback announcements in several property companies, investors took advantage of the opportunity to take profits in these areas. In the country’s bond markets, yields achieved some stability following the previous week’s descent. The yield on the 10-year government bond fell two basis points to close the week at 2.83%. Foreign investors weighed in more heavily on Chinese government and policy bank bonds in July, despite a slowdown in the pace of inflows since January. Expectations were reinforced that the central bank will remain supportive in its liquidity policies, based on a dovish quarterly meeting of the country’s 25-member Politburo on July 30

The Week Ahead

Among the important data scheduled for release in the coming week are Productivity, Unit Labor Costs, and Inflation.

Key Topics to Watch

- Job openings

- NFIB small-business index

- Productivity (preliminary)

- Unit labor costs (preliminary)

- Consumer price index

- Core CPI

- Federal budget balance

- Initial jobless claims (regular state program)

- Continuing jobless claims (regular state program)

- Producer price index

- Import price index

- UMich consumer sentiment index (early)

Markets Index Wrap Up