Monday’s punishing selloff could be the beginning of the next leg lower for stocks as a sense of complacency has taken hold in markets following a stellar October and November, several strategists told MarketWatch.

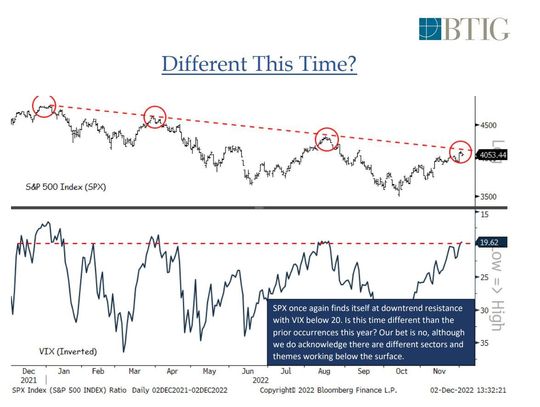

In a note to clients on Monday, Jonathan Krinsky, chief technical strategist at BTIG, said that U.S. stocks were primed to tumble after the S&P 500 SPX, -1.79% bounced off its latest resistance level, which coincided with the index’s 200-day moving average, a key technical level for assets. Krinsky illustrated the pattern in a chart included below.

“Investors have gotten too complacent, as the SPX is turning down from its year-long downtrend resistance just as it did in March and August,” Krinsky said in comments emailed to MarketWatch.

Other market strategists agreed with that warning, but clarified that the sense of complacency has been the result of the market’s powerful relief rally over the past six weeks.

Katie Stockton, a technical strategist at Fairlead Strategies, said the latest pullback for stocks is “a sign that the market is fragile, and reasonably so given the longevity and magnitude of the relief rally.”

Before Monday’s session, the S&P 500 had risen more than 16% off the intraday lows reached on Oct. 13, the day stocks staged a historic turnaround following the release of hotter-than-expected inflation data from September.

After the release of the November jobs report on Friday, stocks slumped again on Monday, with the S&P 500 and Nasdaq Composite Index COMP, -11.01% recording their biggest pullbacks since Nov. 9, according to Dow Jones Market Data. The Dow Jones Industrial Average DJIA, -0.26% and Russell 2000 RUT, -2.78% also sold off sharply.

VIX reflects false sense of security

Traders’ sense of security is reflected in the CBOE Volatility Index VIX, +8.87%, otherwise known as the “VIX” or Wall Street’s “fear gauge,” according to Nicholas Colas, co-founder of DataTrek Research.

Often a counter-indicator, the VIX reaching a sub-20 level should have been a warning sign for investors that stocks were vulnerable to a selloff, Colas told MarketWatch in an email.

“Markets were just too complacent about policy uncertainty and what 2023 holds for corporate earnings. When we get to sub 20 VIX ,it doesn’t take much for markets to roll over,” Colas said in an email.

But as Colas explained, historical patterns have helped to influence the remarkably low level of the VIX over the past couple of weeks.

In theory, seasonal patterns dictate that the rally in stocks should continue into year end, as MarketWatch has reported last week. Typically, stocks rally in December as liquidity thins and traders avoid opening new positions, allowing for what some on Wall Street have called a “Santa Claus rally.”

Whether that pattern holds this year is more murky.

As Colas explained in a note to clients on Monday, the main concern for stocks right now is that investors have been ignoring risks of further downward revisions to corporate earnings expectations, as well as other potential blowback from a looming recession that many economist view as likely.

To be sure, economic data released in recent days points to a relatively robust U.S. economy in the fourth quarter. Jobs data released Friday showed the U.S. economy continued to add jobs at a solid clip in November, despite reports of widespread layoffs by technology companies and banks.

The ISM’s barometer of services sector activity released on Monday rattled markets by coming in stronger than expected. All of this data has stoked fears that the Federal Reserve will need to deliver even more aggressive interest-rate hikes if it hopes to succeed in its battle against inflation.

More aggressive rate hikes could, in theory, provoke a “hard landing” for the economy.

Have falling Treasury yields hit a point of diminishing returns?

As BTIG’s Krinsky explained, a sense of complacency isn’t unique to equity markets. Bond yields also have fallen more than BTIG had anticipated, he said in a recent note to clients, perhaps more than is justified by the uncertain outlook for both monetary policy and the economy.

Since the yield on the 10-year Treasury note TMUBMUSD10Y, 3.594% peaked above 4.2% in October, falling Treasury yields have helped support a range of risk assets, including stocks and junk bonds. The yield on the 10-year note, considered by Wall Street to be the “risk free rate” against which stocks are valued, was just shy of 3.6% late Monday. Yields move inversely to bond prices

Even if yields do continue to fall, the dynamic where lower Treasury yields help boost stock prices may have reached a point of diminishing returns, Krinsky explained.

“While we think this level holds, we wonder if a break under 3.50% would be viewed as equity friendly…[w]e have some doubts,” Krinsky said in a note to clients.

Economists across Wall Street anticipate a recession will begin some time in 2023, expectations that are supported by the steeply inverted Treasury yield curve, which is seen as a reliable recession indicator.

All that has investors keeping a close eye on U.S. economic data for the rest of the week. A report on producer-price growth in November due out Friday could be another major catalyst for markets, strategists said.