Stock Markets

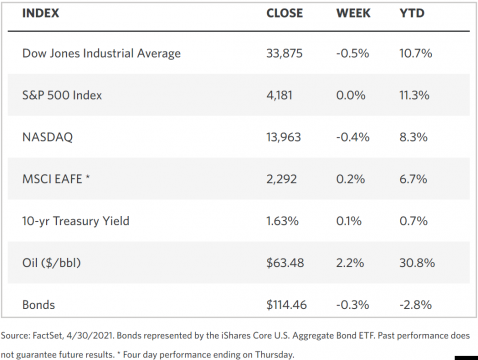

In the past week, stocks tested record highs on the back of positive earnings reports. Although the major indexes closed slightly lower, the S&P 500, Nasdaq Composite, and S&P MidCap all tested new highs prior to correcting for Friday’s close. A deluge of first-quarter reports elicited reactions from investors, causing volatility in the returns of the different sectors. Providing a major buying motivation is the rise in oil prices to their highest level in six weeks. Within the S&P 500, communication services shares outperformed the rest of the counters as a result of earnings and revenue reports from Facebook and Alphabet (parent company of Google). Microsoft’s earnings report exceeded analysts’ expectations; however, this news appears to have been discounted by the market as the stock fell, causing the technology sector to underperform. Health care stocks also fell as a result of the decline of share prices among several drug manufacturers.

U.S. Economy

The strong earnings reports that flooded the market last week are testimony to the robust economic progress the country has made in recent months. At current levels, the S&P 500 is up by 12% compared to the first four months of 2021. Current fundamentals appear to line up with the continuation of a bull market and investor optimism continues to pick up, according to the following indicators.

- The first-quarter GDP rose by an annualized 6.4%, compared to 4.3% recorded in the last quarter of 2020. The recent two rounds of stimulus packages have provided a boost to the economy simultaneous with the continued progress in the vaccination roll-out. Consumer spending surged by 10.7% representing spending of part of the stimulus check. This development is encouraging, since consumption accounts for 70% of the economy. Business investment also increased 9.9%, as well as government expenditure by 6.3%. A reduction in the GDP, however, was contributed by a drop in inventories and exports as a result of the pandemic.

- There have been many earnings reports that have been released in the past week, but these comprise only slightly more than half of the companies in the S&P 500 listing have released news of their earnings. Of those who have reported, about 87% of the companies have exceeded their expected earnings by at least 24%. As already observed, growth stocks such as communication counters (Apple, Microsoft, and Alphabet) will continue to ride the digitalization trends, but even cyclical businesses are bound to realize substantially higher earnings by a wide margin.

- Even though economic activity and employment have admittedly strengthened, the Fed remained unchanged in its conservative policy. There appears to be no change in sight to slow the rate of asset purchases which is currently at $120 billion per month, or to raise interest rates in fear of an inflation rate increase. The Fed’s updated policy framework currently emphasizes average inflation targeting and defines employment gains broadly and inclusively. Given that scenario, it is unlikely that preemptive policies based on economic projections will be instituted. Instead, those crafting policy will wait for the data to confirm any progress substantively made, allowing more time before adopting any major changes. On the other hand, stimulative fiscal policy will continue to be adopted, enabling further growth in the economy. It is possible, however, for growth rates to peak sometime this quarter.

Metals and Mining

The price of gold encountered volatility over the past week as it rose during the week to $1,788 per ounce on Wednesday, April 28, and plummeted to $1,755 the day after. Gold was anticipated to rise above its trading pattern over the past four weeks. It lost steam, however, when the newly released economic data prompted an increase in the 10-year Treasury yields, thus reducing the attractiveness of gold as an alternative investment vehicle. Gold ended the week at $1,768.10 per ounce on Friday, April 30.

Silver continued its downward correction that it had trekked for most of April, even as values this week inched closer to $26.50 per ounce. Despite being closely correlated to gold, analysts feel that it may make a move towards $32 by the second semester of 2021, though it may well average $27.30 for the rest of the year. As of Friday, silver traded at $25.99 per ounce.

The platinum and palladium markets were impacted by the disruption of production in Russia’s Norilsk Nickel (MCX:GMKN), providing an incentive to buy up both metals. Platinum rose on Tuesday to $1,246 per ounce before correcting to $1,182 in later trading. Palladium surged to a new record peak of more than $3,000 on Friday; the metal is a primary material used in the manufacture of catalytic converters, a crucial component that reduces emission in automotive exhaust systems. On Friday, platinum traded at $1,202.25 while palladium traded at $2,882.

In the base metals category, copper breached its 10-year high of $9,990 per tonne, and ended the week at that level, The metal has been consistently trending upward throughout April, rising 11.7% over the last month. Zink began trading for the week at $2,862.50 and ended Friday at $2,928 per tonne. Nickel registered the second largest gain among the base metals, increasing by 5.9% in value by Friday to hit $17,433 per tonne. Lead also went up by 2% for the week to close at $2,097.50 per tonne on Friday, with more upside foreseen in the weeks to come.

Energy and Oil

The price of oil rose gradually through the week but saw a correction on Friday due to profit-taking on the gains made. The sell-out was also likely influenced by concerns about the deteriorating situation in India’s covid outbreak. Oil prices rose to a six-week high on Thursday mainly due to positive economic news in the U.S., in the hopes that the improving economy will increase demand in this country. It is hoped that the growing U.S. demand will offset the bearish outlook of demand from India that would tend to lead to a global oil surplus.

In other countries, the EU carbon prices have exerted pressure on the border tariff. Prices have shot up almost to 50 euro per ton, thus increasing the cost burden on polluting industries. The EU is being called upon by the European industry to overseen carbon border adjustments; this is a tariff imposed on imported products originating from places abroad that have weak climate policy. In Asia, China seeks to replicate, at least in part, America’s shale boom. It is developing its substantial shale gas resources to produce sufficient natural gas to meet its growing demand. Many challenges still have to be met, however, before the country can accomplish even a fraction of the U.S. achievement in this field.

Natural Gas

For the week of April 21 (Wednesday) to April 28, the spot prices of natural gas climbed in most regions. The Henry Hub spot price increased to $2,93 per million British thermal units (MMBtu) from $2.65/MMBtu. At the New York Mercantile Exchange (NYMEX), the May 2021 contract expired April 30, up by $0.23/MMBtu for the week at $2,926/MMBtu. The June 2021 contract price rose by $0.18/MMBtu to $2.960/MMBtu over the same period. The price of the 12-month strip averaging June 2021 to May 2022 futures contracts increased by $0,11/MMBtu to $2.990/MMBtu. Meanwhile, at Mont Belvieu, Texas, natural gas plant liquids composite price went up by $0.21/MMBtu, an average of $7.07/MMBtu for the same week. The average weekly price of natural gasoline slid by $0.01, mirroring the price drop in Brent crude oil price, which suffered the same rate of decrease week-on-week.

World Markets

European shares moved sideways for the week, apparently consolidating after gains in eurozone bond yields caused investors to take profits at close to record high levels. The pan-European STOXX Europe 600 Index closed the week 0.38% down. Major indexes across Europe were mixed. Among those that gained are France’s CAC 40 which rose by 0.18% and UK’s FTSE 100 which grew 0.45%. Those that lost include Germany’s Xetra DAX Index which slid 0.94% and Italy’s FTSE MIB which dipped by 1.00%. Overall, any gains and losses made were minimal as the market did not find any impetus for major moves. Core eurozone bonds, in the meantime, moved higher on speculations that the U.S. Federal Reserve may slow down its bond purchasing program. The release of German inflation data that came out higher than expected also prompted core yields to increase. Yields in the UK and peripheral eurozone bond markets ended higher in tandem with U.S. Treasuries and core eurozone bonds.

In Japan, bourses treaded lower as the Nikkei 225 Index ended down by 0.72% and the broader TOPIX Index fell by 0.87%. The softness in the market became more evident by Friday with the release of worse-than-expected earnings results for some firms trading in the market. The movement also signaled that investors may be adjusting their positions before the Gold Week holiday resumes on May 3-5 when markets close. The yen dipped against the US dollar at JPY 108.9, while yields on the 10-year Japanese government bond gained 0.9%. In China, shares lost ground during the week in view of the government’s crackdown on technology firms. The large-cap CSI 300 Index slid 0.2% and the Shanghai Composite Index dipped by 0.8%. A weaker-than-expected Purchasing Managers’ Index report for April dampened investor appetite for buying. Ahead of the three-day Labor Day holiday, there was little incentive to take a position particularly since some state banks were withholding the release of their 2020 financial results

The Week Ahead

Among the reports scheduled to be released next week are Domestic Auto Sales, the PMI Index, and construction spending.

Key Topics to Watch

- Markit manufacturing PMI (final)

- ISM manufacturing index

- Construction spending

- Motor vehicle sales (SAAR)

- Trade deficit

- Factory orders

- ADP employment report

- Markit services PMI (final)

- ISM services index

- Initial jobless claims (regular state program)

- Continuing jobless claims (regular state program)

- Productivity

- Unit labor costs

- Nonfarm payrolls

- Unemployment rate

- Average hourly earnings

- Wholesale inventories

- Consumer credit

Markets Index Wrap Up