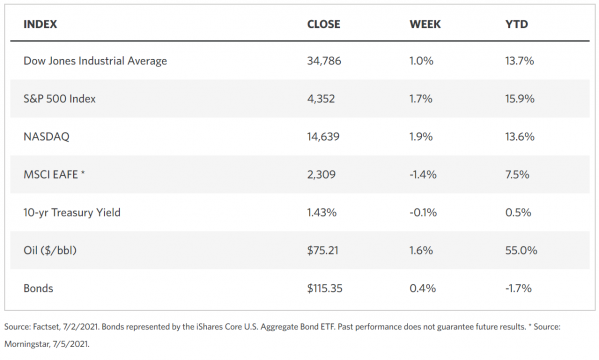

Stock Markets

The stock market gained upward momentum with both the broad S&P 500 Index and the tech=heavy Nasdaq Composite Index closing a fifth successive quarterly rise. The Russell 1000 Growth Index saw an eighth straight weekly gain as large-cap growth stocks led the market advance this week. In the S&P 500, technology and health care stocks outperformed the other sectors although consumer discretionary stocks also showed strength boosted by solid gains in Nike shares. After their strong gains last week, the small- and mid-cap stocks took a respite this week with a minor correction. Although quarter-end rebalancing caused an increase in volumes traded, they remained relatively quiet. A long weekend awaits as the U.S. markets will remain closed on Monday in observance of Independence Day, since July 4 falls on the preceding Sunday.

U.S. Economy

The week saw the announcement of generally positive economic data. The index of consumer confidence performed better than expected as it posted a 16-month high. Surprising gains in housing prices spurred the sentiments of homeowners, and the labor market likewise exhibited robustness that buoyed American optimism about the recovering economy. The Labor Department released a Friday report that 850,000 nonfarm jobs – the most in the past ten months – were added by employers in June; for a change, this bested the consensus estimate of 700,000 by the highest margin since August of last year. The drop in weekly jobless claims was also better than expected, registering 364,000 which is the lowest it has been during the pandemic era. The biggest surprise of the past week was the pending home sales data which surged 8% in May, in contrast with the consensus expectations which bet on a slight decrease. On the low side, factory activity lost some ground by a bit more than expected based on the Institute of Supply Management’s indicator, although the figures still showed a relatively healthy expansion. The factors that impeded faster growth were identified as labor and material shortages.

- Although job gains were a welcome relief, unemployment climbed closer to 5.9% while labor participation remained unchanged. This indicated a failure to meet the Federal Reserve’s threshold for “substantial further progress.” Payrolls for the previous two months were adjusted upward by 15,000, with 40% of the gains contributed by leisure and hospitality, the sectors that lagged the most as a result of the pandemic. Hospitality has much more ground to cover despite outperforming the other sectors in the last five months. From its level in February 2020, employment in this sector is still down by 13%. There is enough momentum for this gap to be covered considering the strong vaccine roll-out, higher consumer savings, and pent-up demand.

- The rosy labor situation notwithstanding, it did little to change the outlook of the Federal Reserve. The Fed’s interpretation of the labor and inflation data is crucial as it will guide the monetary policy they will set out, which is likely to tighten aggressively and earlier than expected. As observed, the employment level remains short of its pre-pandemic level by 6.8 million. The Fed’s parameter for a full, broad-based, and inclusive employment situation, therefore, remains unmet. That being said, there appears to be no urgent reason for monetary tightening measures to be advanced, and the Fed will likely maintain its policy of accommodation for the near future. The speedy pace of job creation will likely encourage policymakers to adopt tapering over the next few months, a reduction in the rate of asset purchasing which is a step towards normalization but far short of tightening.

Metals and Mining

In the week just completed, gold rose slightly by 0.33% to end at $1.787.30 per ounce from $1,781.44. The buying interest in the yellow metal was spurred partly by a weakening of the dollar and investors’ assessment of possible monetary tightening policy by the Federal Reserve. The positive U.S. job report appears to have allayed the fears of a more aggressive policy by the Fed, although some reservations remain as a result of the slight increase in the monthly unemployment rate from 5.8% to 5.9%. Midway through trading, the spot price of gold hit $1,794.86, the highest it has seen since June 18. Another factor that contributed to this market optimism is the increase in U.S. nonfarm payrolls by a larger-than-expected figure at 850,000. The slow rate of coronavirus vaccination roll-out in some parts of the world also appears to have somewhat tempered investor sentiment as some countries in Asia and Europe walked back on their prospects of reopening.

As for the other precious metals, the price of silver increased by 1.42% for the week, ending at $26.47 per ounce from $26.10 the previous week. Platinum saw a slight correction with its close at $1,093.74, down by 1.53% from $1.110.72 per ounce. Palladium chalked in a solid gain of 5.67% with its jump from $2.640.45 to $2.790.29 per ounce. The week’s trading in base metals was mixed with the prices of copper and zinc rising and those of aluminum and tin falling. Copper ended 0.39% down from $9.413.50 to $9.376.50 per tonne. Zinc fell from $2.907.50 to $2.562.00 per tonne, a correction of 11.88%. Aluminum surged from $2.486.00 to $2.935 per tonne, a significant increase of 18.06%. Tin inched upward by 2.42% from $30,774 to $31,520 per tonne.

Energy and Oil

Controversy marked the OPEC+ meeting as the decision expected on Thursday was marred with a delay. The volume of the proposed production increase came at an average monthly addition of 400,000 barrels per day (bpd), which was smaller than the 500,000 bpd expected by industry analysts. Oil prices thus fell on the news. However, the outcome may still be bullish. The UAE delayed the deal as it asked for a higher production quota. This caused some difficulty in the negotiations. The OPEC+ is aware that the other members may protest should the UAE be given the authority to produce from a different base. The group will again confer on Friday.

In the U.S., gas prices reached their highest average level in seven years as motorists faced an extended holiday weekend. Banks have begun to reduce their exposure to the U.S. shale patch, compelling traditional lenders to cut their losses and reduce the risk on their energy loan portfolios. Alternative sources of capital have advanced to take over the U.S. energy debt at a discount and enter into equity or debt transactions that may enable them to realize expedited gains than would a bank loan. In their neighbor to the north, new regulations were announced to effectively prohibit the sale of gasoline and diesel vehicles in Canada in a plan to phase out internal combustion engine modes of transportation by 2035. This mirrors the current trend in Europe where EV sales rose to comprise 11% of all cars sold in 2020 compared to 3% in 2019.

Natural Gas

Liquified natural gas (LNG) prices around the world are seeing their highest levels in years mainly due to the elevated temperatures, particularly in the northern hemisphere. There is increasing demand for power generation to provide for air conditioning, while traders in other regions are beginning to replenish their stocks in anticipation of the increased demand for winter heating. The European gas markets title transfer facility (TTF) reached their peak levels in years, while the JKM marker, an important indicator for the spot market value of cargoes delivered ex-ship into the Asian markets, has jumped above $13 per million British thermal units (MMBtu). The deliveries to the markets in Japan, South Korea, China, and Taiwan constitute the majority of global LNG demand.

During the report week June 23 to June 30, natural gas spot prices rose at most locations. The Henry Hub spot prices increased to close at $3.72/MMBtu from the previous week’s close of $3.33/MMBtu. The July 2021 New York Mercantile Exchange (NYMEX) contract expired Monday at $3.617/MMBtu, an increase of $0.28/MMBtu from the previous week. The August 2021 NYMEX contract prices rose to $3.650/MMBtu, higher by $0.30 over the week earlier. The price of the futures contract for the 12-month strip averaging August 2021 through July 2022 grew by $0.21/MMBtu to $3.429/MMBtu.

World Markets

In Europe, equities were slightly lower due to concerns that inflationary forces may bring about an increase in interest rates. Another dampener on investor sentiment was the news that a highly infectious variant of Covid-19 was spreading and threatened the fledgling economic recovery. The pan-European STOXX Europe 600 Index slid 0.18%, while major indexes were mixed. Germany’s Xetra DAX Index gained 0.27%. Italy’s FTSE MIB Index gave up 0.89% and France’s CAC 40 Index likewise fell 1.06%. The UK’s FTSE 100 Index declined by 0.18%. The core Eurozone bond yields dropped in reaction to news of the spread of the Delta variant in Europe. The European Central Bank (ECB) President, Christine Lagarde, drew attention to the new virus threat and its impact on the economic recovery of the region. The peripheral bond yields followed the cue of the core markets, as well the UK gilt yields. The prospects of U.K. inflation were dismissed by Bank of England (BOE) Governor Andrew Bailey as being temporary, causing gilt yields to further decline.

The Japanese stock market returns slumped for the week also on concerns that coronavirus resurgence may materialize despite the vaccine rollout. The Nikkei 225 Index dropped 0.97% while the broad-based TOPIX lost 0.32%. The yen also declined in value to its lowest point since February of last year, ending the week at JPY 111.43 versus the U.S. dollar. The Japanese 10-year bond yield slid to 0.046%. Since the Olympics are slated for July 23, the government is assessing a possible extension of its July 11 expiration of its coronavirus restrictions. Presently, a quasi-state of emergency is in place as coronavirus cases appear to be trending up. Keeping the restrictions in place will reduce the maximum number of spectators allowed into the Olympic venues to 5,000. A ban is in place for spectators from outside the country, as Prime Minister Yoshihide Suga is prioritizing the safety and security of the Japanese people.

Equities trading for the week was similarly lackluster in China. Weekly losses were posted by both the Shanghai Composite Index and the large-cap CSI 300 Index after a correction from the biggest one-day drop on Friday for each bourse since March. The sell-down was attributed to profit-taking by domestic investment funds and open market operations by the country’s central bank to drain funds from the financial system. Investors were anticipating highly liquid markets leading into the celebration of the ruling Communist Party’s 100th anniversary on Thursday, following a cash injection of the week ahead. There was an increase in the seven-day interbank rate of approximately 30 basis points above the official target, but analysts surmised that this was more a reaction of market pressures at quarter-end and was not necessarily indicative of tighter monetary policy. The People’s Bank of China announced in its latest policy meeting that it would maintain stability in the macro leverage ratio, which suggested that the central bank will forego any plans of tightening policy soon.

The Week Ahead

Looking forward to the coming week, investors can expect the release of the following key economic data: the PMI composite, Consumer Credit, and Domestic Auto Sales.

Key Topics to Watch

- Markit services PMI (final)

- ISM services index

- Job openings

- FOMC minutes

- Initial jobless claims (regular state program)

- Continuing jobless claims (regular state program)

- Consumer credit

- Wholesale inventories

Markets Index Wrap Up