Stock Markets

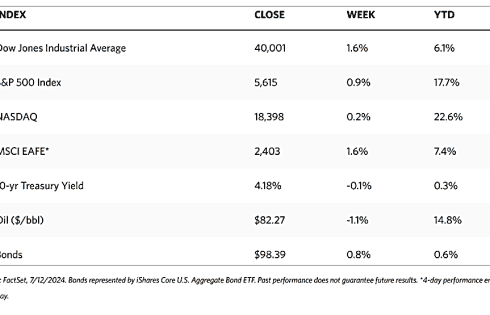

Last week saw the first notably broad advance since mid-April. All major US stock indexes are up for the week. The Dow Jones Industrial Average (DJIA), a narrow 30-stock index, rose by 1.59% while the Dow Jones Total Stock Market climbed by 1.25%. The broad S&P 500 Index increased by 0.87% and the technology-heavy Nasdaq Stock Market Composite rose slightly by l0.25%., although it saw record intraday highs. The NYSE Composite added 2.25%. The risk perception indicator CBOE Volatility Index (VIX) dipped by 0.16%.

The biggest advance was achieved by the small-cap Russell 2000 Index which gained 6.00% making this its best week since early November. While value stocks easily outperformed growth stocks, trading volumes were light over much of the week due to this being the summer vacation season and the fact that investors were awaiting major earnings reports. The official start of the earnings season was on Friday. Second-quarter earnings releases from Citigroup, Wells Fargo, and JPMorgan Chase kicked off the beginning of the season. Analysts expect growth in overall earnings registered by the S&P 500 to surge from 5.9% in the first quarter to 9.3% in the second quarter. This would mark the fastest pace since the first quarter of 2022.

U.S. Economy

Thursday’s release of the Labor Department’s consumer price index (CPI) appeared to be the single major factor market mover this past week. Headline prices fell by 0.1% in June, which marked the first decline of this inflation indicator since the start of pandemic lockdowns in May 2020. Better yet, core prices (excluding food and energy prices which are most volatile) rose by 0.1% which was lower than expected – the slowest pace in more than three years. Chicago Fed President Austan Goolsbee described the data as “profoundly encouraging” as it signaled that inflation was on its way back to the Fed’s annual 2.0% target.

Friday’s producer price index (PPI) data complicated the inflation story and its implications for the market. Headline PPI rose slightly more than expected at 2.0% in June, while May’s reduction was also revised upward to flat. The core PPI reading (excluding food, energy, and trade services), which came in unchanged for the month, seemed to please investors. Consistent with the overall economy, input inflation trends remained concentrated in services, particularly vehicle wholesaling and machinery. In analysts’ view, inflation remains “sticky” in certain key categories. Food inflation has moderated, but it appears to have settled above its pre-pandemic range. Momentum in agricultural prices and the recent uptick in restaurant prices suggest that there remains some upside risk.

Metals and Mining

Investors are wary, based on analysts’ warnings, that the consolidation of the precious yellow metal will come to an end when the market perceives a clear signal from the Federal Reserve that it will ease restrictions in its monetary policy. The week’s developments point to a definite rate cut as early as September. Fed Chair Jerome Powell, testifying before Congress last week, stated that the situation is relatively normal and high inflation is not the only risk to the economy. Gold investors received even more encouraging news after Powell’s comments as core consumer inflation rose at its slowest rate since 2021. Similarly, the US labor market is slowing, This, combined with the easing of inflation pressures, signals the likelihood that the Fed will soon be cutting rates. The current trajectory of the economy shows a clear trend and the labor market has peaked, allowing the Fed enough wiggle room to start cutting interest rates.

The spot market for precious metals ended mixed for the week. Gold climbed by 0.81% from last week’s closing price of $2,392.16 to end the week at $2,411.43 per troy ounce. Silver dipped by 1.38% from its closing price last week of $31.22 to settle this week at $30.79 per troy ounce. Platinum ended this week at $1,003.92 per troy ounce, 2.54% lower than last week’s closing price of $1,030.09. Palladium ended the week at $971.77 per troy ounce, 5.61% lower than its last price a week ago of $1,029.57. The three-month LME prices of industrial metals are also mixed. Copper, which last traded a week ago at $9,944.00, settled this week at $9,786.50 per metric ton, down by 1.58%. Aluminum closed the week at $2,476.50 per metric ton, lower by 2.33% from its last weekly close of $2,535.50. Zinc, which closed last week at $3,001.00, ended this week at $2,959.00 per metric ton, for a loss of 1.40%. Tin gained by 2/34% from its last weekly close of $33,874.00 to end this week at $34,666.00 per metric ton.

Energy and Oil

A slight downward correction for oil prices opened this week as the anticipated impact from Hurricane Beryl turned out to be less damaging than first expected. Constructive macroeconomic data have, however, reversed the initial correction. The fed will likely push through with the September interest cut long expected by the market, with US consumer prices falling for the first time in four years last month. Against this backdrop, ICE Brent rose above $85 per barrel once more. Elsewhere, the International Energy Agency (IEA) foresees weakness in the global demand. The IEA reported the lowest quarterly increase in global demand in over a year as consumption rose by 710,000 barrels per day (b/d) in the second quarter. The report opined that China’s exceptional growth was coming to an end, thus cutting the 2025 outlook further to 970,000 b/d.

Natural Gas

For the report week from Wednesday, July 3 to Wednesday, July 10, 2024, the Henry Hub spot price rose by $0.32 from $2.05 per million British thermal units (MMBtu) to $2.37/MMBtu. Regarding the Henry Hub futures, the price of the August 2024 NYMEX contract decreased by $0.089, from $2.418/MMBtu at the start of the report week to $2.329/MMBtu at the end of the report week. The price of the 12-month strip averaging August 2024 through July 2025 futures contracts fell by $0.077 to $3.001/MMBtu.

International natural gas futures prices declined for this report week. The weekly average front-month futures prices for liquefied natural gas (LNG) cargoes in East Asia fell by $0.08 to a weekly average of $12.49/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands, the most liquid natural gas market in Europe, decreased by $0.13 to a weekly average of $10.51/MMBtu. In the week last year corresponding to this report week (the week beginning July 5 and ending July 12, 2023), the prices were $12.04/MMBtu in East Asia and $9.78/MMBtu at the TTF.

World Markets

European stocks ended the week generally higher. The pan-European STOXX Europe 600 Index gained 1.45%, taking its cue from the US report of lower-than-expected inflation data. Major stock indexes in the region likewise climbed. Italy’s FTSE MIB gained 1.74%, Germany’s DAX rose by 1.48%, and France’s CAC 40 Index added 0.63%. French and German sovereign bond yields fell in tandem with US Treasury yields in response to US inflation slowing down by more than expected. Also falling across most of the curve are UK gilt yields. They ticked up at the very front end, however, as economic growth in May was higher than expected, increasing uncertainty concerning the likelihood that the Bank of England (BoE) would ease monetary policy. Three BoE policymakers expressed reluctance to vote in favor of lower borrowing costs, for which reason the markets have scaled back bets on a rate cut at the BoE’s meeting scheduled for August 1. Chief Economist Huw Pill, Jonathan Haskel, and Catherine Mann, the three BoE rate-setters, indicate that they prefer to keep rates steady until proof emerges that services inflation is poised for a sustained decrease.

Japan’s stocks pulled back at the end of the week from the record highs they reached on Thursday. In the foreign exchange markets, speculation was heightened that authorities intervened to support the yen. The yen surged in value against the US dollar, fueling the speculation of an intervention which was further reinforced by a Nikkei report that the BoJ conducted rate checks after the yen climbed. A strong yen makes Japanese assets more expensive for foreign investors and hurts the profit outlook for Japan’s export-focused industries. As investors assessed the outlook for monetary policy after the yen’s sharp rebound, the yield on 10-year Japanese government bonds (JGB) eased to around 1.05%, a two-week low. As hopes for a US interest rate cut intensified on soft US inflation data, Japanese yields also tracked US Treasury yields lower. In July, the BoJ came under pressure to raise interest rates again to defend the currency and reduce the difference between foreign and domestic bond yields. Regarding the economy, a leading indicator of capital spending in the coming six to nine months, core machine orders, declined unexpectedly for the second straight month in May. The decline is attributable to a sharp decrease in the nonmanufacturing sector. Meanwhile, strong rebounds in the output of motor vehicles, electrical machinery, and other machinery resulted in an upward revision in May’s production growth from 2.8% to 3.6%.

China’s stocks registered gains on the back of strong export data that offset concerns about deflationary pressures. The blue-chip CSI 300 rose by 1.2% while the Shanghai Composite Index added 0.72%. Hong Kong’s benchmark Hang Seng Index surged by 2.77%. In June, exports exceeded forecasts, climbing by 8.6% year-on-year, up from May’s 7.6% growth. The strength in overseas demand was attributed to manufacturers frontloading shipments ahead of potential tariff hikes from several major trading partners. Imports unexpectedly shrank by 2.3% in June, however. This figure is down from May’s 1.8% gain amid weak domestic demand. China’s overall trade surplus rose to USD 99.05 billion, a multi-decade high, from USD 82.62 billion in May. The country’s consumer price index increased by a lower-than-expected 0.2% in June year-on-year, which is narrower than May’s 0.3% rise. Core inflation (excluding food and energy costs) rose by 0.6%, the same as in May. Despite numerous measures to spur growth, China’s economic recovery has been uneven this year, weighed down by the protracted property slump and weak domestic demand that have restrained consumer prices.

The Week Ahead

June reports regarding housing starts and building permits, industrial production, and retail sales data are among the important economic releases in the coming week.

Key Topics to Watch

- Empire State manufacturing survey for July

- Fed Chairman Powell speaks (July 15)

- U.S. retail sales for June

- Retail sales minus autos for June

- Import price index for June

- Import price index minus fuel for June

- Business inventories for May

- Home builder confidence index for July

- Fed Gov. Kugler speaks (July 16)

- Housing starts for June

- Building permits for June

- Industrial production for June

- Capacity utilization for June

- Fed Beige Book

- Initial jobless claims for July 13

- Philadelphia Fed manufacturing survey for July

- U.S. leading economic indicators for June

- New York Fed President Williams speaks (July 19)

- Atlanta Fed President Raphael Bostic speaks (July 19)

Markets Index Wrap-Up