Stock takes a breather as knockout quarter, outlook cap record run while more than half of analysts hike targets

Nvidia Corp. could come to dominate the data center the way Apple Inc. did smartphones, according to one analyst amid several glowing reports from Wall Street after the chip company reported a spectacular quarter and outlook.

Nvidia NVDA, +0.02% shares traded plus-or-minus 2% early Thursday, and closed up 10 cents, or less than 0.1%, at $485.64, following a run where the stock gained nearly 14% in four straight sessions to close at a record $493.48, giving the company a market cap of $300 billion for the first time. Shares are up 106% for the year, compared with an 18% gain in the PHLX Semiconductor Index SOX, -0.89% and a 4.8% gain in the S&P 500 index SPX, +0.31%

Late Wednesday, Nvidia topped Wall Street estimates for both its fiscal 2021 second quarter and its forecast, with data-center sales topping its core gaming business for the first time.

Jefferies analyst Mark Lipacis, who has a buy rating and hiked his price target to $570, likened Nvidia to Apple AAPL, +2.21% in the smartphone era or to the software/hardware duo of Microsoft Corp. MSFT, +2.32% and Intel Corp. INTC, +1.73% in the PC era when it comes to dominating an ecosystem.

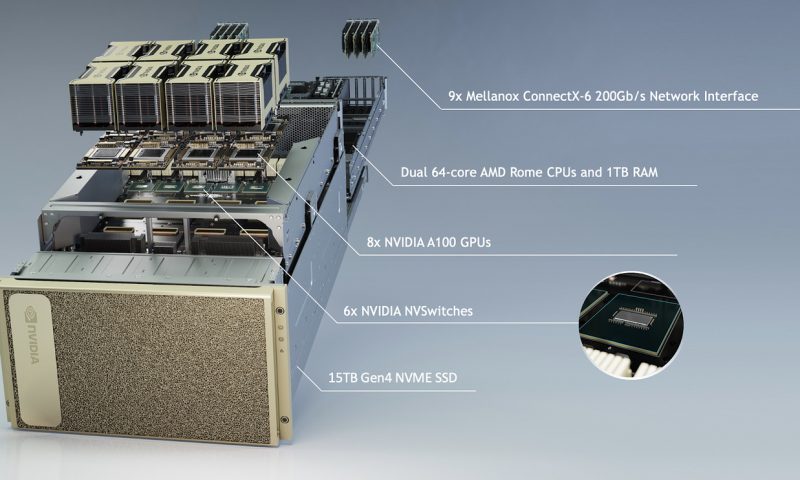

In Nvidia’s case, the ecosystem in question is that of parallel processing, which powers the heart of AI and machine learning. Not only does Nvidia make the graphics processing units that are in high demand at data centers, but those GPUs run on Nvidia’s proprietary CUDA programming platform.

Lipacis said Nvidia “is best positioned to become the de facto standard of the Parallel Processing Era and capture 80% of this ecosystem’s value.”

“We think the company will continue to surprise on the upside, and wouldn’t be surprised to see NVDA undertake more M&A to build out its data center system capabilities,” Lipacis said.

Nvidia just closed its $6.9 billion acquisition of Mellanox Technologies Ltd. this past April, and the first full quarter of having the networking products company on board went a long way.

On Wednesday’s conference call, Chief Financial Officer Collette Kress said that Mellanox contributed about 14% of total revenue on the quarter and more than 30% of data-center revenue, and “was a critical part of several of our major new product introductions this quarter.”

Cowen analyst Matthew Ramsay, who has an outperform rating and hiked his target to $540, questioned whether the “really really really good quarter” for Nvidia was “good enough.”

“We believe Nvidia needed to print a perfect quarter to drive shares higher, and this may be the only bone that gets picked,” Ramsay said. “Looking ahead, we expect a sustainable data-center product cycle that should carry through the remainder of F2021 and F2022, further amplified by Mellanox now fully integrated.”

Gaming, however, may not be in the back seat for long. Ahead of a Sept. 1 event expected to release a new line of gaming chips, Nvidia Chief Executive Jensen Huang said on Wednesday’s call that he thinks “this may very well be one of the best gaming seasons ever.”

Evercore analyst C.J. Muse, who has an outperform ratings and hiked his price target to $600, said he expects both gaming and data center “to sustain excellent growth” all through 2021.

“With shares up 100%+ YTD, some may argue to take profits,” Muse said. “But in the words of Winston Churchill — this is not the end. It is not even the beginning of the end. But it is perhaps, the end of the beginning.”

Of the 40 analysts who cover Nvidia, 32 have buy or overweight ratings, six have hold ratings and two have sell or underweight ratings. With 26 analysts hiking price targets, Wall Street has an average target of $491.39 on the stock, compared with a target of $430.71 before the earnings report, according to FactSet data.