U.S. stock futures on Tuesday were pointing to a poor start to the holiday-shortened week as rising bond yields and geopolitical tensions weigh on sentiment.

How are stock-index futures trading

- S&P 500 futures ES00, -0.84% dipped 36 points, or 0.9%, to 4051

- Dow Jones Industrial Average futures YM00, -0.84% fell 230 points, or 0.7%, to 33640

- Nasdaq 100 futures NQ00, -1.10% lost 154 points, or 1.2%, to 12236

On Friday, the Dow Jones Industrial Average DJIA, +0.39% rose 130 points, or 0.39%, to 33827, the S&P 500 SPX, -0.28% declined 11 points, or 0.28%, to 4079, and the Nasdaq Composite COMP, -0.58% dropped 69 points, or 0.58%, to 11787. U.S. markets were closed on Monday for a public holiday.

What’s driving markets

U.S. investors are returning from the three-day weekend in a downbeat mood.

Trader sentiment is cautious as they observe benchmark bond yields near their highs of the year on expectations recent robust economic data will encourage the Federal Reserve to keep borrowing costs higher for longer.

Minutes of the Fed’s February 1st meeting will be published on Wednesday.

Tensions over Russia’s invasion of Ukraine, as President Joe Biden visits Poland and a Chinese delegation goes to Moscow, are adding to the anxiety.

“So far, risky assets have digested the rates repricing well – while the broad ‘risk-on’ rally has slowed to a crawl, the higher terminal rates have not moved through assets like a wrecking ball as some had assumed,” said Stephen Innes, managing partner at SPI Asset Management.

“But there remains a heightened degree of caution due to the steep rise in U.S. yields and rate volatility, an environment where the U.S. dollar tends to benefit,” Innes added.

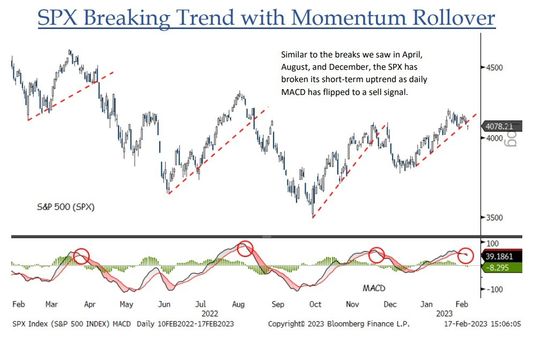

Such caution was matched by Jonathan Krinsky, chief technical strategist at BTIG, who noticed that the latest rally had nevertheless begun to fade.

“After a few weeks of chopping around, the SPX looks to have broken its short-term uptrend just as momentum has begun to roll over, similar to breaks we saw in April, August, and December of 2022,” Krinsky wrote in a note to clients.

“As a reminder, the back-half of February is often one of the weaker parts of the calendar. This has come on the heels of rates which have been moving higher for the last couple of weeks. A slow equity reaction to rates has not been atypical over the last 18-months, as each of the prior six tactical peaks all occurred one to four weeks after the low in rates,” he added.

U.S. economic updates set for release on Tuesday include the S&P flash services and manufacturing purchasing managers’ indices for February, due at 9:45 a.m. Eastern. Existing home sales figures will be published at 10 a.m.

Walmart WMT, +1.50% and Home Depot HD, -1.02% are among the companies set to report earnings.