After a period of post-pandemic hibernation, where growth was uneven, one closely watched measure of biopharma R&D productivity is moving in the right direction. According to the 16th edition of Deloitte’s annual Measuring the Return from Pharmaceutical Innovation report, which is tellingly titled “Navigating the GLP-1 boom,” the projected internal rate of return on late-stage pipeline assets rose for the third consecutive year, hitting 7.0% in 2025. That’s a jump from 5.9% the year before. The sector, it seems, has transitioned from winter to spring. “We went through a period of so many years where the returns kept declining, excluding the COVID impact in the middle,” said Kevin Dondarski, principal for life sciences strategy at Deloitte Consulting. “But the increase over the last few years is analytically unprecedented.”

The catch? Much of that growth in 2025 traced back to a single class of therapies. GLP-1/GIP drugs targeting obesity and related metabolic conditions now account for an estimated 38% of all projected commercial inflows from the 2025 late-stage pipeline. Strip them out, and headline internal rate of return (IRR) falls from 7.0% in 2025 to 2.9%. For the sake of comparison, IRR was 5.9% in 2024 and without GLP-1/GIP drugs, it was 3.8%. “There are two different messages here,” Dondarski said. “One, it’s certainly attractive, because the market is valuing the potential impact that those therapies can have on the public, which is great. But at the same time, it raises the question of sustainability. As those programs progress, is there going to continue to be that opportunity through the next generation and the next? It will create a responsibility for these companies to find the right assets to replace in the pipeline.”

When asked if removing one drug class had ever flipped the direction of the headline IRR number, Dondarski said this year was the most dramatic example the report has ever seen over its 16 year history. “There tends to be a certain set of classes that account for a lot of value; if you take them out, the IRR goes down. But this is the largest impact that I think we’ve seen in the history of our work.”

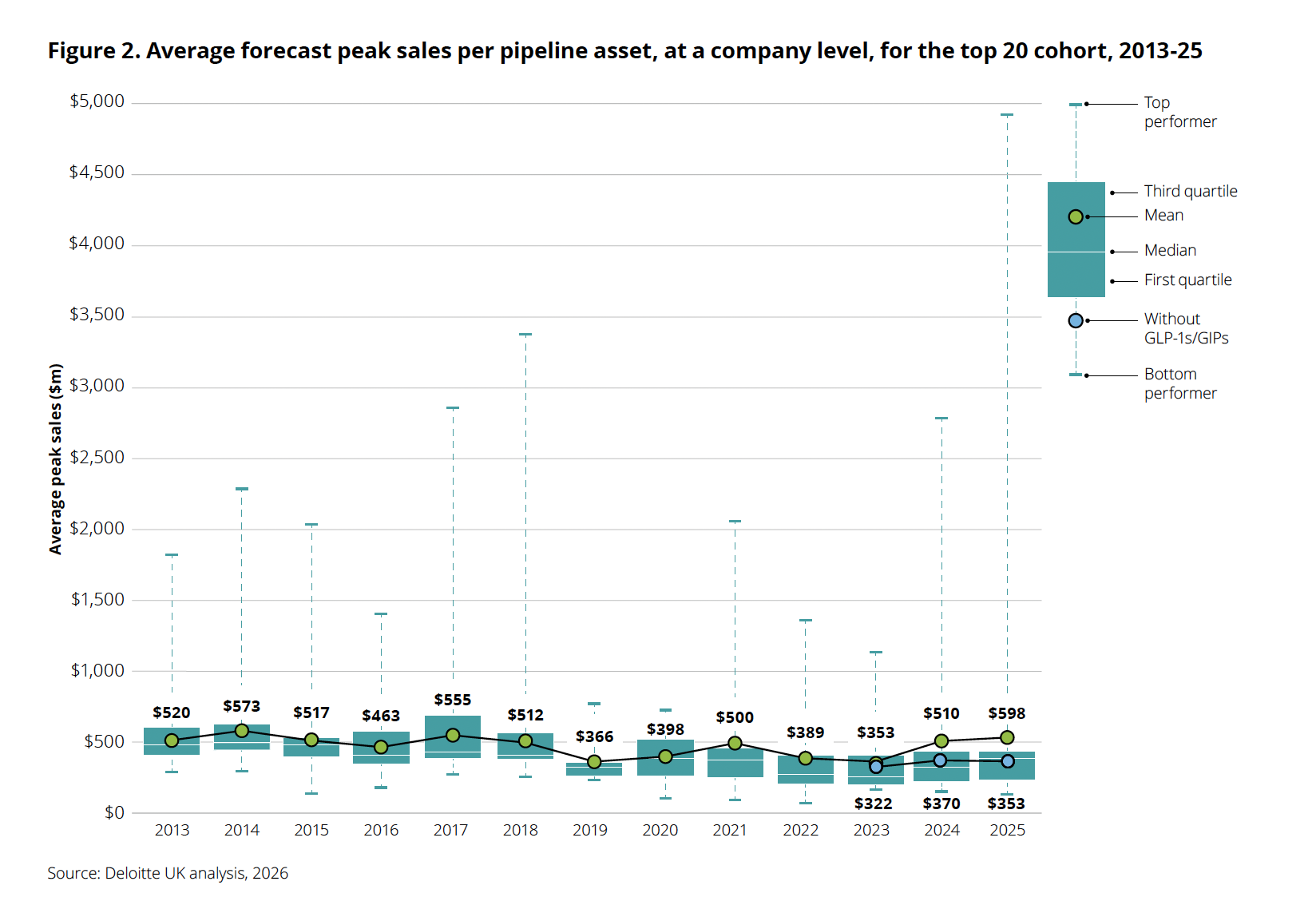

Average forecast peak sales per pipeline asset jumped to $598 million in 2025, but the spread tells the real story: the top performer now approaches $5 billion while the “without GLP-1s/GIPs” marker sits at $353 million, actually lower than the year before. Strip out the obesity blockbusters and underlying pipeline productivity is declining. Source: Deloitte, “Navigating the GLP-1 boom,” 2026.

Investors have been getting mixed signals about the durability of the GLP-1/GIP boom. Since the beginning of the year, tirzepatide (marketed as Zepbound and Mounjaro) developer Eli Lilly, which launched its oral GLP-1 orforglipron (marketed as Foundayo) in April 2026, has seen its stock skid roughly 10-13% year-to-date, even as it raised full-year revenue guidance to $82-$85 billion on the strength of Mounjaro and Zepbound volume growth. In 2025, Novo Nordisk swapped longtime CEO Lars Fruergaard Jorgensen with Maziar Mike Doustdar amid slowing momentum and share-price pressure. Seven board members stepped down at a November 2025 extraordinary general meeting, and the company announced plans to cut about 9,000 roles from a global workforce of 78,400. Novo’s Q1 2026 release says the company employs about 67,900 employees, implying roughly 10,500 fewer than the 78,400 workforce cited when the restructuring was announced. Adding to the pressure, Novo had hoped CagriSema, a combination of the amylin analogue cagrilintide and semaglutide, would drive future growth. Instead, the drug failed to show non-inferiority against Lilly’s Zepbound in the REDEFINE 4 Phase 3 head-to-head trial reported in February 2026, delivering 23.0% weight loss versus 25.5% for tirzepatide, triggering another wave of investor disappointment.

Are obesity drugs the golden goose?

Despite the turbulence, strong demand for GLP-1s persists. Lilly delivered a clean Q1 beat, while Novo’s quarter showed a more complicated version of strength: rapid Wegovy pill uptake and a profit beat alongside lower adjusted sales. Lilly reported revenue of $19.8 billion (versus $17.6 billion expected), a 56% year-over-year increase driven by Mounjaro at $8.7 billion (+125%) and Zepbound at $4.1 billion (+79%). Lilly raised full-year revenue guidance by $2 billion, to $82-$85 billion. Novo reported Q1 sales of DKK 96.8 billion ($15.2 billion), with its oral Wegovy pill, launched January 5, generating DKK 2.26 billion in its first quarter, nearly double the DKK 1.16 billion analysts had expected. But the underlying tension persists: Lilly’s 56% revenue growth was driven by a 65% volume increase partially offset by a 13% decline in realized prices, and Novo’s adjusted sales still fell 4% at constant exchange rates once a one-time $4.2 billion 340B provision reversal was excluded.

On top of all of this, both Eli Lilly and Novo Nordisk have agreed to lower U.S. prices for GLP-1s through Medicare, Medicaid and TrumpRx. Under the November deal, Medicare and Medicaid coverage for weight-loss use was expected to expand for the first time, with $50 monthly copays for eligible beneficiaries. The live TrumpRx site now lists Wegovy pill at $149 per month, Wegovy pen at $199, Ozempic at $199 and Zepbound at $299.

The spiraling cost of R&D

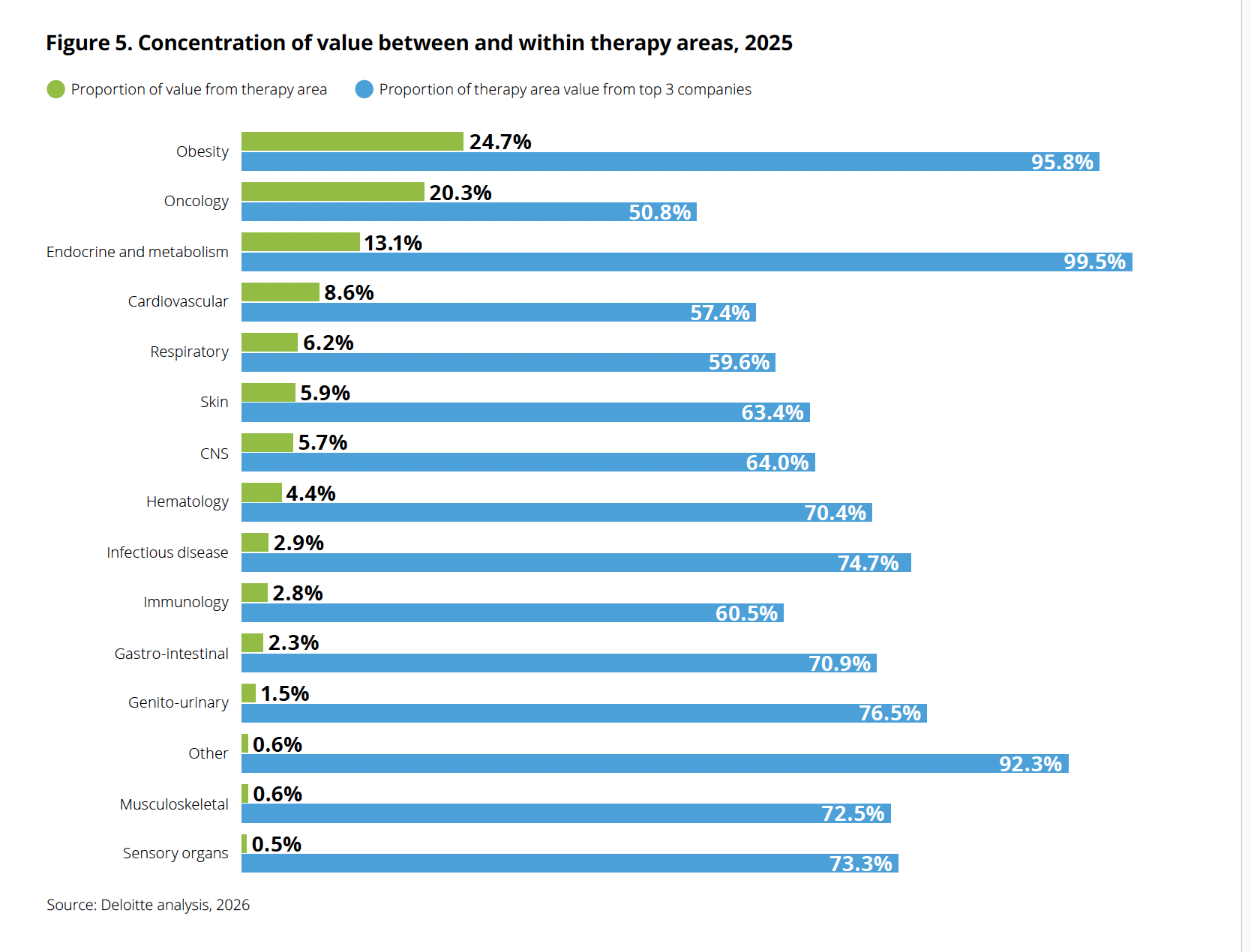

Obesity now commands the largest share of late-stage pipeline value (24.7%), displacing oncology (20.3%) for the first time in the report’s 16-year history. But the concentration within obesity is even more striking: nearly 96% of that value sits with just three companies. Source: Deloitte, “Navigating the GLP-1 boom,” 2026.

The report also found that the average cost to develop a drug from discovery to launch grew to $2.67 billion in 2025, up from $2.23 billion the year before. Dondarski said the team investigated whether a single outlier explained the spike. “We saw the cost increase for 17 out of the 20 companies, so it was a persistent theme,” he said. Three factors converged, including R&D costs continuing to rise above general inflation, large-scale M&A deals inflating the R&D cost base, and attrition shrinking the overall number of late-stage programs by roughly 4-5%.

AI: still waiting for liftoff

Last year’s edition of the Deloitte report was titled “Be brave, be bold” and urged pharma companies to embrace AI-powered drug development platforms, automation and advanced analytics as a path to reversing decades of declining R&D productivity. Despite that call to action, the 2025 data shows R&D costs climbing to a record $2.67 billion per asset while clinical cycle times remain stubbornly long. The report now concedes that AI’s promise to significantly reduce development time and costs “has not yet been realized at scale, largely due to a pilot-driven, function-by-function approach.”

That is not to say AI experience is for nought. “Everybody’s actively focusing on AI, and everybody’s had some degree of success,” Dondarski said. “But from our vantage point, there’s a good amount of variability in the velocity at which organizations are scaling those efforts to maximize value creation.”