The continued expectations of easing monetary policies

across the globe buoyed stocks higher this week. After the Fed chairman’s

testimony before Congress, the Dow Jones Industrial Average rallied to a new

record high and closed above 27,000. Powell’s comments were clearly aimed at a more

accommodative policy that strengthened expectations for a rate cut on the

horizon. The European Central Bank (ECB) is also reiterating this sentiment and

is considering injecting fresh stimulus to the economy via interest-rate cuts,

or the possibly quantitative easing. As the second-quarter earnings season

kicks off next week, attention will shift from central banks moves to earnings,

which analysts believe may increase volatility.

U.S. Economy

The U.S. economic expansion seems set to continue in good

stead. In his words to Congress this week, Chair Powell characterized the

economy as “in a good place.” Many endorse the fact that our current economic

expansion has endured largely because of moderate pacing of economic growth.

The economy’s steady pacing is supported by solid consumer spending, which

composes 70% of economic growth. Based on strong unemployment, modest wage

growth, and low interest rates, consumers are expected to maintain the current

positive trend. As always, there are risks to this optimistic outlook:

Too low of inflation

Inflation running either too high or too low

is a negative. In the current climate the more immediate risk to the bull

market is too low inflation more commonly called deflation. The risk here is

that deflation could trigger a recession. The Fed has shown its willingness to

cut short-term interest rates to correct this.

U.S.- China trade tensions

Trade tensions between the U.S. and China are

a major factor with the potential to slow global growth by dampening business

investment and disrupting supply chains. According to OECD (Organization for

Economic Co-operation and Development), world trade growth for 2019 has fallen

to 2.1% in 2019 from 3.9% in 2018. Trade tensions play a major role.

Slowing global growth

While trade tensions are currently stealing

headlines, other global concerns can be worrisome. These are based around

geopolitical uncertainties such as Brexit, burgeoning Italian debt, and a slowing

Chinese economy. All these factors have contributed to a slowing of global

growth. Based on current trends, analysts expect global economic growth to slow

over 2019.

Metals and Mining

The gold market had solid gains for the week with prices

holding above critical psychological level at $1,400 an ounce. Gold also

benefited from Fed Reserve Chair Jerome Powell’s comments before Congress,

which indicated a rate cut on July 31. A softer US dollar, geopolitical issues

and a slow in economic growth were the main drivers behind the precious metal’s

ability to trend between US$1,270 and US$1,420 per ounce throughout the

quarter. August gold futures last traded at $1,418.60 an ounce, up more than 1%

since last Friday. Next week will test endurance for gold bulls, as they wait

to see if prices can hold above $1,400 an ounce in what should be a relatively

uneventful week.

Silver made slight gains of 1.26 percent over the second

quarter of this year which just came to a close. The white metal was somewhat

stagnant throughout the period, but on a positive sentiment note, it reached

its highest level towards the end of June.

Energy and Oil

Global oil demand continues to soften, which analysts say

could result in a supply surplus in the second half of this year. The EIA

downgraded its forecast for global oil demand growth to just 1.1 million

barrels per day (mb/d) this year, down from the 1.2 mb/d the agency forecasted

last month and from 1.4 mb/d in May in its latest Short-Term Energy Outlook.

They say that the “increasingly weak outlook” for demand could upend global

balances. A slowing economic picture now means that inventories could actually

increase by 0.1 mb/d. So, even with the OPEC+ cuts extended, the oil market

could remain in a state of surplus throughout this year and next.

Natural gas spot prices rose at most locations this week.

Henry Hub spot prices rose from $2.24 per million British thermal units (MMBtu)

last Wednesday to $2.46/MMBtu Friday. At

the New York Mercantile Exchange (Nymex), the price of the August 2019 contract

increased 15¢, from $2.29/MMBtu last Wednesday to $2.444/MMBtu Friday. According

to Baker Hughes, for the week ending Tuesday, July 2, the natural gas rig count

increased by 1 to a total 174. The number of oil-directed rigs fell by 5 to a

total of 788. The total rig count decreased by 4, and it now stands at 963.

World Markets

Stock markets in Europe fell even as continued signs that

both the Fed and the European Central Bank (ECB) are endorsing further stimulus

measures. The pan-European STOXX Europe 600, the UK’s FTSE 100 Index, the

German DAX index, and France’s CAC 40 Index fell as trade tensions expanded to

a U.S. and France dust up. The European Commission cut its eurozone growth and

inflation estimates citing the fact U.S. trade policy could pose a risk to the

group. The commission lowered its inflation rate increase expectation, which it

believes will be further from the ECB’s target of close to, but less than 2%

over all.

Stocks in China recorded a weekly loss, likely as the U.S.

trade policy’s impact on China’s economy sunk in. The benchmark Shanghai

Composite Index fell 2.67%, and the large-cap CSI 300 Index, gave up 2.16%.

China reported that export growth in June slowed 1.3% from a year ago, while

imports fell a bigger-than-expected 7.3% from the prior-year period.

Even as a temporary halt in the trade battle was reached

between the U.S and China, analysts believe that the differences between the

two countries are complex and are not easy to resolve. This leaves the risk of

increased tariffs and other forms of retaliation to potentially escalate

quickly if negotiations break down.

The Week Ahead

This week kicks off the second-quarter earnings season when

about 10% of S&P 500 companies report earnings all week long. Key economic

data coming this week include retail sales, industrial production numbers,

housing starts, and the index of leading economic indicators report, along with

consumer sentiment released Friday.

Stocks managed to extend their recent gains, even with a

shortened holiday week; the S&P 500 closed near its record high. All investors

felt relief after the U.S. and China agreed to suspend new tariffs and resume

negotiations with no specifics. While that was the expected course, the fact

that the leaders were able to avoid further escalation of trade tensions and

move away from heightened tensions was still viewed as very positive. Another

positive emerged as 10-year government bond yields fell to their lowest levels

in more than two years based on signs of slower U.S. growth and expectations of

additional easing by the central bank.

U.S. stocks may have been the beacon that is leading the

way, however international equities are also up double-digits this year, as

well as small-cap stocks. Analysts suggest that as the cycle advances,

well-diversified portfolios will be better positioned to navigate the swings

and keep investors on track toward positive momentum.

U.S. Economy

Markets seem convinced that there is room for 2019 to

continue to its end with a positive outlook. But they caution that there’s more

bumps in the road ahead. The first half of the year’s highs in stocks and low

interest rates, combined with last week’s data provide key takeaways: last

week’s employment report showed that the U.S. economy added 224,000 new jobs in

June, the strongest month this year and solidly above the 161,000 average so

far in 2019. Monthly payroll gains averaged 223,000 for all of 2018, so the

current slowdown in hiring raises fears that the U.S. economy is heading toward

recession. The Fed’s apparent willingness to consider rate cuts in an effort to

extend the economic expansion lends strong support.

The S&P 500 rose by a strong 17.4% (18.5% including

dividends) in the first six months of 2019. Again, that’s the single best first

half year since 1997. There has been a total of 10 years during the last 60 when

the stock market returned more than 15% in the first half. For a full seven of

those 10 years (70%), the market also posted a positive return in the second

half of the year. The stock market finished positive for the full year in all

10 of those years averaging a 27% return.

Metals and Mining

Gold investors have to be enjoying this run as gold remains

one of the strongest precious metals and continues on track for its seventh

straight week of gains. As the week ended,

gold dipped over 1 percent on Friday, precipitated by the US

dollar strengthening ahead of the release of US jobs data.

Analysts say they see the dollar a tad stronger and the euro

weak, which usually holds gold back. Unfortunately, the readiness to push

prices higher by speculators is also pretty limited.

Silver was down over 1 percent on Friday but could make a

rebound based on indications that the Fed will cut interest rates later this

month. Market watchers seem to remain positive about the silver, despite its

current relatively stagnant nature. Analysts forecast that the silver price

will average US$16.20 per ounce in Q4 of this year before rising to an average

of US$17 in the fourth quarter of 2020. The other precious metals were mixed

with platinum down nearly 2 percent for the week and palladium tracking as the

only precious metal to make gains early in the session on Friday, ticking up

0.06 percent. As of 9:00 a.m. EDT, the metal headed for its fifth straight week

of gains, trading at US$1,557 per ounce.

Energy and Oil

OPEC and allies gathered this week in what most felt was one

of the least heated meetings in recent years, rolling over their production

cuts into March 2020. This send signals that the oil market is still over supplied,

and demand growth looks weaker for the balance of 2019.

If successful, OPEC’s mission to draw down excess

inventories would lead to higher oil prices. Its cartel members need this

action to balance their budgets, which are overly reliant on oil exports.

At the same time, higher oil prices are helping U.S. shale

production to continue growing which is directly offsetting a lot of supply

that OPEC is withholding from the market. OPEC and its Russia-led non-OPEC

partners in the production cut deal are focused on reducing inventories and

boosting prices. OPEC’s ‘free pass’ to U.S. shale is not expected to last long,

according to JP Morgan. The cartel and its largest producer, Saudi Arabia will

reclaim market share from U.S. shale, JP Morgan’s head of EMEA oil and gas

research Christyan Malek reported to the media this week.

Natural gas spot prices fell at most locations this week.

Henry Hub spot prices fell from $2.36 per million British thermal units last

Wednesday to $2.32/MMBtu Friday. At the New York Mercantile Exchange, the July

2019 contract expired Friday at $2.291/MMBtu, up 2¢/MMBtu from last Wednesday.

The August 2019 contract remained unchanged Wednesday to Wednesday at

$2.268/MMBtu.

World Markets

The pan-European STOXX Europe 600 Index, the UK’s FTSE 100

Index, and exporter-heavy German DAX index all rose throughout the week

surrounded by increased hopes that the European Central Bank (ECB) will

continue to provide monetary stimulus to keep the region’s economies moving

forward. Both stocks and bonds got a bump after International Monetary Fund

(IMF) Managing Director Christine Lagarde was nominated to be the next ECB

president. Markets believe that she will continue the monetary policy

established by current President Mario Draghi.

In Germany, data punctuated the cost that trade tensions

mixed with slowing global growth have had on its export-dependent economy.

German industrial orders were reported lower in all sectors, dropping 2.2% in

May and for a total of 8.6% for the year. Overall, this is sharpest

year-on-year drop of industrial orders since 2009.

Chinese stocks posted a weekly gain as a reaction of relief

to a temporary cease-fire on tariffs struck by President Trump and Chinese

leader Xi Jinping last week. The absence of any further specifics about when or

how resumption will take place tempered optimism about long term solutions. The

benchmark Shanghai Composite Index added 1.1%, and the large-cap CSI 300 Index,

gained 1.8%. Chinese stocks rose immediately after Trump and Xi met at the G20

summit in Japan and agreed to restart talks alongside the U.S. suspending any

new tariffs on Chinese goods.

The Week Ahead

It’s a relatively quiet week on reports with a few important

indicators coming out including the NFIB small business index report on

Tuesday, FOMC meeting minutes released on Wednesday and inflation plus weekly

jobless claims reported on Thursday. The producer price index will also come

out this week.

Stocks finished mixed this week as markets took in the

strong gains from the month of June. Investors were in a wait-and-see mode

anticipating Friday’s G20 Summit in Japan. The big takeaway would be a trade

truce and resumption of negotiations between the U.S. and China, which stalled

last month. The week also marked the end the quarter and the first half of

2019. At the year’s midpoint, we reached an important milestone: the 10-year

anniversary of the current economic expansion. Of course, some volatility crept

in during the second quarter 2019, but the markets remained strong with rising

bonds and stocks adding to gains. While this expansion might be the longest,

analysts still believe that there is room to run for some time.

Two large mergers of note happened this week. Eldorado

Resorts says it will acquire Caesars Entertainment in a deal worth about $17

billion, making the pair the largest U.S. gaming company. Drug maker AbbVie has

agreed to acquire rival Allergan for around $63 billion in cash and stock.

U.S. Economy

As we end the 2nd quarter, the current U.S. economic

expansion logs in as the longest-running one on record, going back to 2009 and

surpassing the 1991-2001 expansion. Obviously, the quality and characteristics

of the economy have evolved over time, but can this expansion continue even

further? Most analysts are in agreement that it can, but they caution that they

don’t believe the next stage will look the same as this current phase. Expansions

have typically finished with the end of a bubble, such as housing or tech, from

an external shock or based on poorly conceived monetary policies. None of these

are at play at the moment. The good news for investors is that bull markets

rarely end without an accompanying recession. This expansion is by most

estimates performing well enough continue to offer support to the stock market

going forward.

Metals and Mining

Gold has been on a tear this month and now gold markets are

testing if the precious metal can hold support above $1,400. There is continued

and persistent selling pressure after hitting its six-year high this week.

Market sentiment is clearly bullish as prices pushed to a

six-year high, but by week’s end, sentiment took a more reserved stance since

analysts are questioning aggressive expectations for lower U.S. interest rates

that came out of last week’s Fed meeting. Gold’s gains have also been largely

supported by expectations of an interest rate cut in July by the Federal

Reserve.

So, although Gold is off its highs, it is still experiencing

its best month in three years. Gold prices are up almost 1% for the week and up

nearly 8% for the month. Silver was also on track for a monthly gain, but then

moved down slightly on Friday. As of 12:30 p.m. EDT, silver was trading at

US$15.25 per ounce. The other precious metals remain strong, with platinum

inching up to US$838 per ounce and palladium closing out the week US$1,518.50

per ounce.

Energy and Oil

Oil prices moved higher at the end of this week, like other

markets anticipating the meeting between Donald Trump and Xi Jingping. The

sentiment is of course that talks could result in a breakthrough in trade

negotiations, an agreement to resume talks, or a collapse and subsequent

increase in tariffs. All of these will affect oil prices. OPEC kicks off its

meeting in Vienna on Monday. Market bulls will be hoping that the G20 summit

will provide a trade breakthrough while the supply side of oil continues to show

bullish signals, according to market insiders.

Natural gas spot prices fell at most locations this report

week. Henry Hub spot prices fell from $2.36 per million British thermal units

(MMBtu) last Wednesday to $2.32/MMBtu yesterday. According to data from

PointLogic Energy, total U.S. consumption of natural gas rose by 4% compared

with the previous week. Natural gas consumed for power generation climbed by 8%

week over week based on slightly warmer than normal temperatures in the US

southeast.

European governments are reported to be “doubling down” on

efforts to keep economic ties with Iran, in an effort to keep their nuclear

deal alive. The EU has tried to develop a financing mechanism to bypass U.S.

sanctions, but most foreign companies are unwilling to do business in Iran

under the current heated climate.

World Markets

The pan-European STOXX Europe 600 Index, the UK’s FTSE 100

Index, and the exporter-heavy German DAX Index all rose slightly throughout the

week based on expectations that the Group of 20 summit would help ease global

trade tensions. One soft spot was the yield on the 10-year German bond, which

fell to -0.34% as European economic indicators were disappointing.

Chinese stocks were off slightly for the week as traders

were moving cautiously in advance of a much-anticipated meeting between

President Trump and his Chinese leader Xi Jinping at the G20 summit. The

benchmark Shanghai Composite Index declined 0.8% and the large-cap CSI 300

Index lost 0.2%. However, for the month of June both indexes rose off of

positive signals on trade earlier in the month. The Shanghai benchmark rose

2.8% and the CSI 300 Index gained 5.4% in June based on optimistic investors

expecting the G20 meeting between both leaders would, at least lead to the

resumption of trade talks that halted last month.

The Week Ahead

It’s a shortened week for U.S. financial markets with banks

and markets closed on Thursday for the U.S Independence Day holiday. Canada

will close its banks and markets on Monday for their Independence Day

celebrated July 1st. Major economic news includes the ISM manufacturing

Purchasing Managers’ Index, May factory order numbers, auto sales reported on

Tuesday and June’s jobs report released on Friday.

This is the third straight week that U.S. stocks finished

higher. Both the S&P 500 and the Dow closed at new record highs. The clear

driver for the for the rally in both bonds and stocks was the Federal Reserve

releasing news that it is open to rate cuts this year – possibly as early as

next month. The committee dropped its statement about being patient in setting

rates, which had signaled it would hold rates steady for some time. Instead, it

now states it will act as appropriate to sustain the economic expansion.

Following the financial crisis of 2008, the U.S. stock market first achieved a

new record high in 2013. It has now set 225 all-time highs, validating the fact

that new highs can’t be viewed as a single indicator of exhaustion. It’s

important to note that periodic dips in the market provide a good opportunity

for long-term investors to expand diversity in their portfolios by adding

high-quality assets at lower prices.

U.S. Economy

In the first quarter, the U.S. economy grew at a solid 3.1%,

but showed some signs of weakness. Consumer spending dropped to half its

average rate and when combined with a lackluster jobs report and slowing wage

gains set the stage for potential slowdown. This week though, the Fed

demonstrated to the markets its willingness to cut rates in order to head off

rising risks from deflation, trade threats and a slowing global economy. Markets reacted swiftly as the U.S. 10-year

Treasury yields dropped to 2.0%, but rebounded to 2.06%. U.S. rates are low but

still higher than most developed countries. So, it is likely that foreign demand

for U.S. Treasuries will help keep long-term rates low and analysts expect it

to prolong the bull market by providing inexpensive credit to businesses and

consumers.

Metals and Mining

It looks like the patience of gold bulls has finally paid

off. This week, demand for the precious metal managed to drive prices to levels

we have not touched on in nearly six years. Gold climbed 2 percent on Friday

morning (June 21), rising above US$1,400 per ounce to reach as high as

US$1,410.78 at one point. The driver for the surge is obviously the Fed

delivering its dovish opinion that the market was seeking. Essentially this has

removed the ‘patience’ approach to cutting rates,” that the Fed has echoed all

year. Some analysts feel gold’s major breakout could be just the start of a

long-awaited rally as investors strongly expect a shifting interest rate based

on a cut that could come as early as next month. Gold saw most of its gains

this week following the Federal Reserve’s monetary policy meeting.

Silver followed gold’s lead once again proceeding the Fed

announcement, but in the end gave up 1.2 percent of its gains. In the other

precious metals group, platinum was down nearly 2 percent for the week. On Friday

morning, the metal was trading at US$799 per ounce. Like the others, palladium

rallied up 1.43 percent for the week, but edged down just over 1 percent on

Friday. As of 9:43 a.m. EDT, palladium was trading at US$1,487 per ounce, still

higher than gold.

Energy and Oil

Oil prices spiked up about 5 percent on Thursday as the U.S.

announced out was considering a military strike against Iran. The U.S. military

seemed poised to carry out a strike late Thursday, but the operation was called

off by President Trump at the last minute. Reuters reported that Trump may have

relayed a message to Iran that he was seeking to open negotiations. Friday

morning Trump tweeted that he called off the strike because it would not be

proportional to the shooting down of an unmanned drone. His tweet reads “I am

in no hurry, our Military is rebuilt, new, and ready to go, by far the best in

the world. Sanctions are biting & more added last night. Iran can NEVER

have Nuclear Weapons, not against the USA, and not against the WORLD!,”.

Still, this had the whole region on alert. Iranian sources

told media that the Supreme Leader was opposed to negotiations. They also said

that any attack would have regional and international consequences. As the week

closed oil prices were set for their largest weekly gain since February. Natural

gas spot price movements were mixed this report week. Henry Hub spot prices

remained flat at $2.36 per million British thermal units. At the New York

Mercantile Exchange, the price of the July 2019 contract decreased 11¢, from

$2.386/MMBtu last Wednesday to $2.276/MMBtu Friday. The price of the 12-month

strip averaging July 2019 through June 2020 futures contracts declined 9¢/MMBtu

to $2.442/MMBtu.

World Markets

Equity markets rose this week on expectations of added

stimulus. European stocks rose, mostly fueled by anticipation of more central

bank stimulus measures. The pan-European STOXX Europe 600 Index, UK’s FTSE 100

Index, the exporter-heavy German DAX index, and Italy’s FTSE MIB Index all

gained. This followed an announcement by ECB President Mario Draghi that the

bank could offer more stimulus measures as early as July. Draghi’s comments

came prior the Federal Reserve’s commitment that it is ready to cut rates if

the U.S. economic outlook does not improve.

The euro fell about 1% against the U.S. dollar on the week

while the yield on 10-year German government bonds fell to a new all-time low

of -0.315%, and the yield on the French 10-year bond hit 0%, its lowest level

ever. The British pound rose almost 1% against the U.S. dollar, in part led by

the Bank of England’s (BoE) decision to hold short-term rates steady at 0.75%.

With positive momentum across all markets, the Chinese

stocks advanced for the week. Traders are betting that a meeting between U.S.

President Trump and his Chinese counterpart Xi Jinping at this week’s G20

meeting in Japan would put the two countries back at the trade table, which

halted last month. The benchmark Shanghai Composite Index gained 4.2% and the

large-cap CSI 300 Index, added 4.9%. Both indexes recorded their largest weekly

gains since the week ended April 5, according to Reuters.

Sentiment toward Chinese stocks also picked up after the Fed

left its key rate unchanged and signaled that it was ready to lower short-term

interest rates for the first time since 2008.

The Week Ahead

Important economic news to come out this week ranges from

consumer confidence to global influence. The Conference Board’s consumer

confidence report comes out on Tuesday followed by the important durable goods

orders numbers on Wednesday. To cap off the week, the University of Michigan

issues its sentiment report on Friday. The very important G20 Leader’s Summit

kicks off in Japan beginning Friday. President Trump and Chinese leader Xi have

said they will to meet separately in a session aimed at resolving important

issues hanging up trade negotiations between the two global powers. The outcome

will certainly send messages to global markets.

The week was pretty quiet with stocks edging higher and in a

bright spot, small-cap companies outperforming. There were a number of

high-profile mergers that lifted investors’ confidence this week, but indexes

gave back some gains on Friday, likely due to chipmaker Broadcom’s announcement

that the U.S./China trade tensions are suppressing demand. On Thursday, following

attacks on two tankers near the Persian Gulf, oil attempted a brief rally, but

finished out lower pressured by worries about sinking global demand for oil.

Retail sales reports showed a rebound in U.S. consumer spending in May that

followed a relatively slow first quarter. This is solid evidence that consumers

are still well-positioned. In a snapshot, all major indexes have rebounded to

near all-time highs – a very positive outlook with some expectations of higher

volatility by analysts.

U.S. Economy

The real driver in the 10-year U.S. economic expansion is

consumer spending. In fact, it accounts for a full two-thirds of overall GDP.

Consumption spending averaged 2.6% growth in 2018 and then fell to half that

rate for the first three months of 2019. That’s because seemingly strong GDP

was propped up by temporary factors like inventories and imports. The release

of the lackluster May jobs report and slowing wage gains last week compounded concern

that consumer spending might be weaker than analysts thought.

That is why this week’s retail sales numbers are being

closely monitored as an indicator of consumer health and market strength. In

the end, it was very good news, with May retail sales stronger than expected.

That was followed by news that the previous months’ retail figures were revised

higher. So, all told, retail sales suggest that consumer spending rebounded in

the second quarter to a healthy 3.5%. That’s even higher than in 2018.

Tariff Concerns Linger

The ongoing elevated trade tensions between the U.S. and

China have added to market concerns that economic growth could be slowed due to

increasing tariffs. A clear indication of the sentiment followed news of

progress towards a trade deal earlier this year, which triggered a rally in

share prices. With negotiations between the U.S. and China at a kind of

impasse, it seems that trade tensions are taking a toll on both countries.

China’s industrial production sank to 17-year lows in May, and U.S. industrial

production has also suffered in recent months, while it did manage to rebound

marginally in May.

Metals and Mining

Precious metals were fueled by ongoing trade war concerns

this week between the US and China, alongside some wavering global equities.

Gold was flat on Friday after making gains in the previous

session. That was pushed by the US dollar dropping from the two-year peak it

hit on Wednesday and global equities declining due to increased China-US trade

tensions.

Sentiment is turning bullish for gold as prices broke

through critical resistance, pushing to their highest level since early-April

2018. Analysts are warning that gold could face a short-term setback this week

after the Federal Reserve’s monetary policy meeting.

Gold’s continued four-week rally is seen as a result of

aggressive market signals that the Federal Reserve will loosen monetary policy

with a first cut coming in July. According to the contrarians, the market’s

fortunes could shift if the Fed doesn’t meet the market’s expectations.

Silver followed gold’s lead on Friday and dipped slightly

after climbing over 1 percent in the previous session. Industry experts still

believe in the silver’s potential, however. Firms polled in a key report from

FocusEconomics echoed that silver could reach as high as US$17.80 per ounce by

end of year. Platinum made small gains on Friday after reaching its lowest

level since February and stayed on track for its fifth straight weekly loss.

Palladium made the most gains on Friday, ticking up over 1 percent and once

again entering into US$1,300 per ounce territory.

Energy and Oil

The big energy news was oil prices surging early Thursday

after two oil tankers were reported to have been hit by explosions in the Gulf

of Oman between Iran and the United Arab Emirates (UAE). That’s just one month

after a previous incident in Middle Eastern waters. The U.S. has video proof,

CENTCOM says, that Iran was behind the explosions that rocked the two tankers

in the Gulf of Oman.

Immediately following the event, WTI Crude was surging 3.17%

at $52.76, while Brent Crude was soaring 3.42% at $62.02. However, at week’s

end, oil finished its stand lower forced back down by worries of lower global

demand for oil.

On the natural gas front, mild weather and record U.S.

natural gas production kept prices low despite low storage levels and high

exports. On June 6, the price of the Henry Hub natural gas near-month futures

contract at the New York Mercantile Exchange (NYMEX) closed at a three-year low

of $2.324 per million MMBtu. That is its lowest price since May 31, 2016.

Following on June 11, the spot price of natural gas at the Henry Hub closed at

$2.34/MMBtu, the lowest price since November 17 according to Natural Gas

Intelligence.

World Markets

As was widely expected, Mexican assets rallied early in the

week in response to Mexico’s immigration-related agreement with the U.S.,

reached late last week in order to avoid new tariffs.

European stock markets ended the week slightly higher,

pushed by the rise in oil prices that stemmed from the tanker incident in the

Gulf of Oman. They are under pressure from U.S.-China trade tensions and weak

industrial data coming out of China. The pan-European STOXX Europe 600, the

UK’s FTSE 100 Index, the exporter-heavy German DAX index, and Italy’s FTSE MIB

Index were all gainers.

Japan’s GDP figures were revised upward: for the quarter

ended in March, Japan’s gross domestic product annualized growth rate was

increased to 2.2%. That’s up from the 2.1% estimate a month ago. Sources in the

Cabinet Office say this was due to upwardly revised capital spending data.

Chinese stocks rebounded as traders’ confidence increased

that Beijing will make efforts to step up stimulus measures that could help

cushion the economy from any impact from U.S. tariffs. The benchmark Shanghai

Composite Index ended up 1.9%, an eight-week high. The large-cap CSI 300 Index,

which tracks blue chips listed on the Shanghai and Shenzhen exchanges, added

2.5%. These gains come just one week after both indexes closed at their lowest

levels in nearly four months.

The Week Ahead

There are a couple of key drivers that will light up the

headlines this week in the markets: first and foremost is a rate decision from

the Federal Reserve that comes out on Wednesday. Another important focus will

be the U.S. housing data, which details housing starts and building permits in

a report issued on Tuesday, with existing home sales released this coming

Friday. Tensions are increasing in China and could see more unrest in Hong Kong,

where protesters are planning more demonstrations.

The S&P 500 rallied 4.4% as stocks finished higher for

the best weekly gain in the last six months. However, bond yields declined to

the lowest levels in nearly two years. Increased expectations of a Fed rate

cut, positive response to the U.S. and Mexico reaching a resolution to avoid

tariffs, and improved valuations, all helped stocks move higher.

In terms of economic data, signals were mixed with strength

from the services sector mostly offset by weakness in the manufacturing sector.

While job gains for the month of May came in below expectations, the

unemployment rate is still very healthy at a 50-year low. Analysts expect a

more balanced mix of positive and negative moves this season and feel confident

about rising corporate profits, strong economic growth, combined with low

interest rates creating a positive fundamental base that outweighs risks.

This also offers an opportunity to enhance diversification.

Reviewers call for appropriate global stock-market allocations, with

diversification across asset classes, including small- and mid-cap stocks, that

will likely benefit from increased trade fears or renewed economic signals.

U.S Economy

There remains continued evidence of a slowdown in the U.S.

economy, which in turn boosted hopes for a turn in Fed’s policy. Numbers from

ADP showed that private sector payrolls had grown by the smallest monthly

amount in over nine years for the month of May. Alongside that news, the Labor

Department reported overall, payrolls had expanded by only 75,000 in May. The

saving grace: May’s unemployment rate held steady at of 3.6%, its lowest in

five decades. Almost immediately after the figures were issued, futures markets

began pricing in over a 98% probability of a rate cut in 2019, which they say

has a 90% chance taking place by July (source: CME Group data).

Economist suggest that ultimately, the determination of

whether the economy continues to grow or falls into recession will be

determined by the labor market and household spending. By most estimates, these

are expected to remain healthy enough to support moderate GDP growth this year.

This is heavily weighted in favor of the still-healthy labor market that is

driving several key metrics.

Mexico On Hold

Expected tariffs planned to come into effect on June 10th

were averted in a last-minute deal reached between the U.S. and Mexico. In a

joint declaration released by the U.S. state department, the two countries said

Mexico would take “unprecedented steps” to curb irregular migration

and human trafficking.

The U.S. did not however, get one of its key demands that

would have required Mexico to take in asylum seekers heading for the U.S. and

process their claims on its own soil.

Mexico agreed to:

Deploy up to 6,000 additional troops along

Mexico’s southern border with Guatemala using its National Guard beginning

Monday

Take “decisive action” to tackle human

smuggling networks

The US agreed to:

Expand its program of sending asylum seekers

back to Mexico while they await reviews of their claims.

“work to accelerate” the adjudication

process

Both countries have offered pledges to “strengthen

bilateral co-operation” over border security, including what they have

called “coordinated actions” and information sharing.

These actions, while not inferring a long-term solution,

have arrested the immediate actions of the intended tariff going into place and

offered some signs of confidence that the two parties can work out terms that will

give the markets breathing room.

Metals and Mining

The precious metals markets were given a lift this week by

geopolitical issues that continue to plague investors who then seek out the

metals as safe havens. At the forefront was the gold market, which saw its best

weekly performance in more than a year. Some leading analysts have predicted

that the precious metal has enough momentum now to snap the critical long-term

resistance barrier in the near-term. Lower U.S. employment growth helped push

gold prices back to within close breaking distance of the all critical $1,350

level. During the week, August gold futures traded at $1,347.10 an ounce, up

2.7% compared to the previous Friday.

Gold faces some strong technical headwinds. Since hitting

its 2015 low, it has tested resistance at or near $1,350 a total of eight

times. Silver is taking some signals here, following gold’s lead on Friday. It

added gains on the back of ongoing geopolitical concerns too, trading just

under the US$15 per ounce level on track for its best week since late January.

The others in the precious group were also up: platinum was up close to 1

percent for the week and on track for its first weekly gain in the last seven

weeks. Palladium also climbed, edging up 1.05 percent for the week. As of 10:05

a.m. EDT Friday, palladium was trading at US$1,346 — a gain of close to US$20

from the previous week.

Energy and Oil

Once again, energy shares lagged, weighed down by continued

weakness in oil prices, and the typically defensive utilities and real estate

sectors also underperformed. Oil futures climbed for a second straight session

Friday, with U.S. prices erasing their loss for the week just two days after

dipping into a bear market. Natural gas spot prices fell at most locations this

week. Henry Hub spot prices fell from $2.63 per million British thermal units

(MMBtu) last Wednesday to $2.39/MMBtu. Temperatures were close to normal across

much of the Lower 48 states, with warmer-than-normal temperatures in the

Pacific Northwest and cooler-than-normal temperatures in the Southwest and

Northeast. At the Chicago Citygate, prices decreased 22¢ from a high of

$2.43/MMBtu last Wednesday to $2.21/MMBtu yesterday. Traders will be watching

updates on a production-cut agreement between the Organization of the Petroleum

Exporting Countries (OPEC) and other major oil producers ahead of the deal’s

expiration at the end of this month.

World Markets

European stocks rose as investors began pricing in

expectations for rate cuts as both the U.S. Federal Reserve and the European

Central Bank (ECB) indicated that they could possibly intervene if trade

tensions hit the global economy. The pan-European STOXX Europe 600 Index and

the UK’s FTSE 100 Index gained more than 2%. The exporter-heavy German DAX

Index and Italy’s FTSE MIB Index both gained almost 3%. Germany, which leads

European economies, reported that its Bundesbank data showed weak exports are

taking a toll on the German economy and cut its economic output forecast to

0.6%, down from 1.6% in December. The central bank also slightly lowered forecasts

for 2020 and 2021. Meanwhile, signs of China’s slowing economic growth

continued to accumulate. Clearly this is raising hopes for stimulus from

Beijing. The International Monetary Fund trimmed its 2019 growth forecast for

China to 6.2% from a prior 6.3% estimate and projected 6.0% growth next year.

The Week Ahead

This coming week is a relatively light week for reporting,

but some areas to focus on include inflation numbers to be released on

Wednesday, along with May retail sales and consumer sentiment reported this

coming Friday.

Stocks declined for the 4th straight week impacted by rising

trade tensions and continued geopolitical uncertainty. With the White House

announcing that the U.S. will impose tariffs on Mexico in order to quell

illegal entry, concerns increased on unresolved U.S.-China trade issues. These

have a serious impact on global growth. May showed the largest stock market pullback

this year, but in counterpoint, bonds rallied significantly. Overall, both the U.S. and global yields

showed declines; the 10-year Treasury ended at its lowest point in 21 months at

just 2.13%. German yields followed suit moving into negative territory.

U.S Economy

The leading US economic news surrounded the proposed tariffs

on all imports from Mexico in a bid to force Mexico to deal with its illegal

immigration problem. It’s hard to tell if higher tariffs on China and Mexico

are short-term tactics aiming to spur on specific actions, or they are more

long-term strategies that could stay in place after any goal is achieved. Both

of those things have occurred in past tariff bouts. Higher tariffs on U.S.

imports generally lead to higher prices in the U.S. and slower economic growth

for the countries involved. But the impacts are also typically small when

compared to the overall U.S. economy. Most analyst are still looking at

economic growth to continue at 2% to 2.5% in 2019. That’s thanks to strong job

numbers, slowly rising wages, low inflation, low interest rates and aggressive

fiscal policy.

Tariffs on Mexican Imports

The surprise tariff increase on Mexican imports is a 5%

tariff slated to begin June 10 and to increase monthly to cap at 25%. The plan

is to pressure Mexico over its inaction in dealing with stopping illegal

immigration flows to the U.S. Leading imports from Mexico include autos and

electronics, with the overall import figure at about $350 billion. Stocks in

the leading sectors declined in response. It’s hard to tell if these tariffs

will prompt a response from Mexico, but most analysts don’t expect tariffs to

rise to 25% on imports from Mexico. However, ongoing threats of higher tariffs

and trade disruptions are expected to add to stock market volatility.

Metals and Mining

The gold market is living up to its potential as a

safe-haven asset this week with prices pushing back above $1,300 an ounce. Gold

is seen as attractive because it is considered one of the cheapest safe-haven

assets out of all the financial markets. The U.S. dollar index has struggled to

hold gains above 98 points, but it continues to trade near a two-year high.

Meanwhile, the U.S. 10-year bond yields are trading at around 2.16%. The

inverse is true for gold, which is trading at a two-week high. The August gold

futures last traded at $1,309.20 an ounce. That is up over 1% from last week.

Geopolitical tensions always come to bear on the metals markets, and especially

gold. Some analysts think they have reached a tipping point with President

Donald Trump adding a 5% tariff on Mexico in his efforts to halt illegal

immigration into the U.S.

Energy and Oil

U.S. oil futures dropped by more than 5% on Friday to settle

at their lowest since February as another market saw affects of the Trump

administration’s plans for tariffs on Mexican goods. The concern is that the

tariffs may affect economic growth and therefore, energy demand. Overall,

energy shares performed worst for the second consecutive week as domestic oil

prices tumbled to their lowest level since February. The prices were dragged

lower by a smaller-than-expected decline in U.S. crude inventories. In a move

not widely reported, the Trump administration has decided to approve expanded

use of ethanol fuel. That is expected to help corn farmers hurt by the trade

conflict with China. According to data from PointLogic Energy, the average

total supply of natural gas rose by 1% compared with the previous week. Dry

natural gas production grew by 1% compared with the previous report. Average

net imports from Canada were down 2% from last week.

World Markets

This week, both the U.S.-China trade tensions and President

Trump’s new plan to impose tariffs on Mexico pushed equity markets in Europe

down as investors moved to lessen risk. The pan-European STOXX Europe 600 fell

about 2%, the UK’s FTSE 100 lost about 1.6%, and the export-heavy German DAX

index dropped 2.4%. Tensions are increasing in Italy between the euroskeptic

government and the European Union (EU). As a sign, the FTSE MIB Index lost

almost 3%. Investors sold Italian government debt likely due to growing fears

of a showdown between Rome and Brussels over Italy’s high debt levels. Over the

week, the benchmark Shanghai Composite Index added 1.6%, and the large-cap CSI

300 Index added just under 1%. The CSI 300 is notable as it tracks all bluechip

stocks listed on the Shanghai and Shenzhen exchanges.

The Week Ahead

There’s plenty of economic data to watch this week: the

Manufacturing Purchasing Managers’ Index comes out, along with auto sales and

construction spending from the month of May. A bigger factor will be May’s jobs

report, which will be released this week, with most market watchers and

economist expecting the unemployment rate to stay right in line with the

cyclical lows.

Key Topics to Watch

• Mexican Tariffs by the US • China Trade War with the US • ADP National Employment Report • U.S. International Trade in Goods & Services Report • ISM Manufacturing Report on Business • Revised Productivity & Costs

The fact that US stocks finished the week lower seems to

weigh on concerns that U.S. trade tensions with China are expected to be

prolonged. The broad sentiment across economic reports suggest that global

growth is showing signs of slowing. Lower oil prices pushed energy stocks down,

but utilities came back to lead advancing sectors. This is a “normal” seasonal

shift since it’s common for sector leadership to alternate from over time. For

investors, this reinforces why it’s important to ensuring your portfolio is

diversified across different sectors with variations in risk.

U.S Economy

The US economic figures are continuing strong; perhaps the

strongest we have seen to date. A snapshot of the key figures tells the story

pretty well. The US is about to tally the longest economic expansion yet. Based

on current figures, the streak of positive U.S. GDP growth will pass the 1990s

expansion to become the longest on record in June. As for unemployment, the

country is at a 50-year low. At 3.6%, the unemployment rate has fallen from 10%

a decade ago to its lowest level since the late 1960s. The US markets are on

their second-best all-time bull market. In the current run, the market has

gained more than 400% from its lows in 2009. The only previous bull market to

overtake this stretch was the 1987-2000 run that was both the longest and

strongest.

Actions by The Fed

The US Fed continues to help moderate the markets as it has

for nearly a decade. Despite tariff war worries, geopolitical issues and global

uncertainties, the Fed has stayed steady. What was a late-2018 sell-off then

became a strong 2019 rally thanks mostly to the Fed’s pivot to a more friendly position

on interest rates. The release of the Fed’s recent meeting minutes last week

proved that the U.S. central bank is holding off on additional rate hikes for the

immediate future. Since the economy is growing modestly with low inflation, the

Fed’s policy makes sense. But because the market that has gotten used to the

Fed’s defensive position, any policy shift viewed as a negative could be a

potential market risk. Investors then are eyeing allocation to some bonds as a good

defense.

Metals and Mining

It wasn’t a great week for gold bugs, as the gold market has

essentially given up all its earlier gains and is preparing to end the session

at a near a two-week low. The week started out positive week for gold as

investors moved into safe-haven assets likely due to the across-the-board 2%

drop in equities. But that was short lived with gold prices looking to end the

week down nearly 1% since last Friday. June gold futures last traded at 1275.90

an ounce. Certainly, some bears are pushing the renewed bearish sentiment for

the precious metal expecting that the momentum of strong equities could push

prices to a new low for the year in the near-term. Platinum made small gains on

Friday after reaching its lowest level since February 15 and palladium made the

most gains on Friday, ticking up over 1 percent and once again entering into

US$1,300 per ounce territory.

Energy and Oil

Natural gas has been inching higher as above normal

temperatures are coming into view. Ending the week, crude oil settled 11 cents

lower at $62.76 as OPEC considered easing production cuts amid escalating

Middle East tensions. Equity markets finished the session on a down note as

investors were reluctant to push stocks higher with uncertainty surrounding

trade negotiations. Analysts believe natural gas will likely remain locked in a

narrow trading pattern as strong production and mild temperatures chip away at

the global storage deficit.

World Markets

Trade worries are certainly front and center for global

markets. Negotiations have stalled and the threats of additional retaliatory

tariffs between the US and China are in play again. Last week’s U.S.

manufacturing and durable goods orders indicate that activity slowed recently.

This has again increased fears that trade turmoil is beginning to show up in

the entire economy. When U.S.-China trade tensions escalated in 2018, markets

absorbed sharp sell-offs and enjoyed serious rallies. The same has occurred as

of late, possibly linked to some positive signs on broader trade with the U.S.

dropping retaliatory tariffs with Canada and delaying auto tariffs with the EU.

Manufacturing and trade are important, but they are not the central driver of

U. GDP. That number is driven by consumer spending. As an important side note,

the British pound fell against the U.S. dollar but rebounded slightly after

embattled UK Prime Minister Theresa May announced that she would resign on June

7 given her inability to get her Brexit deal approved by the British

Parliament.

The Week Ahead

The coming week will be shortened by the Memorial Day

holiday in the US. Look for second-quarter gross domestic product (GDP) which

is slated for Thursday, and both consumer spending data and the University of

Michigan Consumer Sentiment Index will be released on Friday.

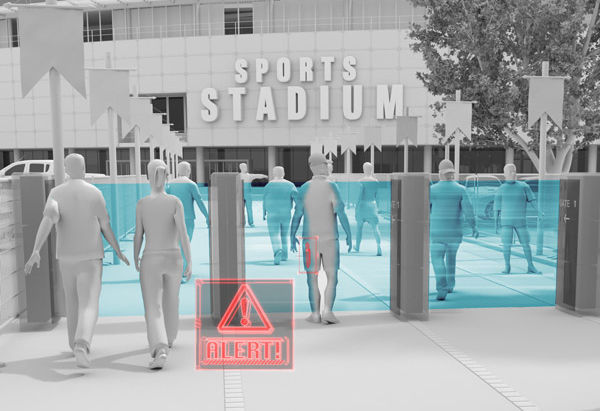

Walking into any concert venue, sports arena, or secure government building today, and the first thing you now must do is empty your pockets and walk through a metal detector. Thanks to a rise in mass shootings and terror alert levels, this clumsy and cumbersome process has slowly become the new normal for any entry into a busy place.

However, this era of slow security entry may finally be

coming to an end, as the future of security could soon merely involve a casual

stroll through a gate that safely and swiftly scans waves of people in real

time.

Meet HEXWAVETM from Liberty Defense Technologies – a brand new threat detection technology developed

at MIT that uses real-time Active 3D Image processing to detect metallic and

non-metallic threat objects and location, such as a gun, or guns, carried near

a school or place of worship prior to the criminal even entering the building. The

detection system, can now be as overt as a typical screening gateway, or covert

as installing devices into the walls or other hidden fixtures on the way into

the venue.

“What we’re targeting is the urban security market,” said

Bill Riker, CEO of Liberty Defense in an interview

with WIRED.

Developed to provide a key part of a layered threat

detection defense Liberty Defense is

looking beyond airports to other scenarios where people need to be scanned

quickly and unobtrusively—such as concerts, sporting events, and large outdoor

gatherings.

Upon detection, the system can tie into security

infrastructure to instantly begin setting off alarms, locking doors and putting

people inside on alert to enhance safety in a scenario where every second

counts.

“What we’re offering is an attack prevention system,” said Liberty

Defense COO and President of US Operations, Aman Bhardwaj, in

an interview with Forbes. “We’re preventing someone with a weapon from

entering.”

Speed + Stealth =

Safety

The Liberty Defense Technologies HEXWAVETM system

is the racing to become the security protection of the future—and it couldn’t

come soon enough.

Since 2015 there have been over 1,700 mass shootings in the

USA, with an average of over 350 shootings happening per year. In high-traffic

scenarios, dense gatherings of people are soft targets. Currently there are no

means to counter threats beyond entry point solutions, which have limitations

in terms of a combined criteria for accuracy, throughput and even location around

or within the perimeter of a facility.

Beyond just sporting events and concerts, places like

hotels, schools, and places of worship tend to have a lot of patrons always

entering and exiting.

A system such as HEXWAVETM might have prevented a

scenario such as the Las Vegas shooter successfully bringing a cache of weapons

up to his room, veiled under common luggage pieces. HEXWAVETM is

designed to discreetly spot metallic and non-metallic objects of interest, such

as guns or other weaponry.

Tourism

in Las Vegas took a noticeable hit in the aftermath of the shooting atrocity.

Hotels have been forced to look at new methods to protect their patrons, while

refraining from installing obtrusive gate of entry checkpoints that would

further add to the feeling of uneasiness left after the horrible event.

Where HEXWAVETM aims to help such venues, is to

utilize discreet hidden sensors amid entry points, that could perhaps be hidden

behind posters, in hotel furniture or in the light fixture—allowing people to

be scanned unaware. Through communication from the sensors to central controls,

a tripped alarm could alert police or local security officers, while giving its

clients instant notification in order to act accordingly, based on the

information provided by the scanners.

Advanced Privacy

Much of the resistance towards security systems, such as

those employed by the TSA in airports and terminals, is directed towards the

intrusiveness of their nature. Privacy

advocates and civil libertarians have raised concerns about some of the

more prominent systems in places such as Dulles International Airport, where

facial recognition scanners are in use.

“Right now, there is very little federal law that provides

any type of protections or limitations with respect to the use of biometrics in

general and the use of facial recognition in particular,” said Jeramie D.

Scott, national security counsel for the Electronic Privacy Information Center

in an

interview with the Washington Post. Scott’s organization has

filed Freedom of Information Act requests seeking details about the program.

Unlike visual recognition technology that is currently in

use at many venues, the HEXWAVETM offers a much less intrusive

solution.

This is achieved by several “game changing” advancements in

the technology, which were developed at MIT Lincoln Labs and are exclusive to

Liberty Defense Technologies.

Due to its unique antenna design and embedded computing

power, HEXWAVE’sTM creates 3D

images that are virtually analyzed in real time using an artificial

intelligence architecture.. The system’s advanced antenna design provides the

capability for the sensors to be distributed

in a way that is covert. Further, the

modular, self-contained design can be deployed across the entry paths of a

venue thus enabling it to be scalable to the needs of a responsive security

operation.

Personnel for Rollout

Beyond developing an effective technology, the challenge for

stakeholders such as Liberty Defense Technologies is to get their system into

as many venues as possible. Key to the company’s future successes are the

people behind the scenes.

Bill Riker was brought on as CEO in August 2018, after a

storied career with Smiths Detection, DRS Technologies, General Dynamics, and

the US Department of Defense. COO and President of US Operations, Aman Bhardwaj

compliments Riker’s security background, with a tech and manufacturing career

that includes over 20 years of experience working with leading global teams for

both major and startup companies, including Panasonic, Flextronics/Imerj, Educo

and Hisense.

Riker and Bhardwaj are joined by a highly-qualified

management team of leaders from the security industry, product development,

government technology and manufacturing sectors. Assisting the management team

is a highly experienced advisory board.

Notable among the advisory board is Francesco Aquilini,

owner of the Vancouver Canucks NHL hockey team, and the team’s home, Rogers

Arena which seats nearly 19,000 people. Aquilini also sits as the team’s main

representative on the NHL Board of Governors, among a group that has at least

13 arenas privately owned by members of the board.

Aquilini is not the lone sports presence on the advisory

board, as current President of Concacaf (the continental soccer governing body in

North and Central America) Victor Montagliani is also advising the company. As well, John May, former member of the Live

Nation Canada management team, helped grow that event promotion company through

to a successful joint venture with Maple Leaf Sports and Entertainment—owners

of all the major professional sports teams in Toronto (NBA, NHL, MLB, MLS,

CFL).

Meeting Demand

Liberty Defense has an exclusive license with MIT and a

Technology Transfer Agreement with MIT Lincoln Laboratory for active millimeter

imagining technology originally developed in the MIT Lincoln Laboratory for

weapon detection. They are continuing to

support the effort through a cooperative research and development agreement for

both the commercialization of the design and that includes other development to

continue progressing the technology.

This capability was developed. in

response to the growing threat from terrorism, especially after a wave of

subway and train attacks witnessed around the world in places like Madrid and

London. Prior to the HEXWAVETM innovation,

it was practically impossible to develop security systems with existing

technology for busy public spaces without grinding pedestrian traffic to a near

halt.

The demand is there: According to a Homeland Security

Research Corp. study, the global explosives and weapons systems market is

projected to be more than $8 billion by 2020 and more than $11 billion by 2025.

Liberty Defense Technologies is targeting the urban security

which generally consists of 4 vertical markets.

The market is segmented into four

verticals that include public venues, secured perimeters and buildings, land

transportation and a category called “other” that includes everything from

schools through places of worship, hospitality fclities and even

hospitals. Thesehave been projected to

reach $1.5-$2.0B in North America by 2020.

Projections for each component include: Public Venues

($283-$428M, CAGR to 8.8%); Secured Perimeters ($820M-$1.03B, CAGR to 4.7%);

Land Transportation ($174-$257M, CAGR to 8.2%); Other/Schools/Hotels

($201-$228M, CAGR to 2.7%).

In late 2018, Liberty Defense Technologies secured a C$7

million fundraising, in order to commercialize the HEXWAVETM system.

“The response from the investment community has been

overwhelmingly positive,” said Bill Riker, CEO of Liberty Defense. “There is

real commitment to solve the issues surrounding public safety that have

proliferated in recent years, and this detection system offers an innovative

approach for this challenge with the HEXWAVE product.”

Demand

for Electric Vehicles (EVs) is sharply on the rise, leading to initiates both

private and publicly-backed to incentivize an electric revolution on the roads,

including a $50 billion pledge from

Volkswagen to embark on an electric car ‘offensive’.[1]

In the United States, there are currently

approximately 840,000 EVs on the road, according to the Edison Electric

Institute’s report from June 2018. Between

Q1 of 2017 and Q1 of 2018, sales increased 32%.[2]

The proportionate number of EVs on the road is set to increase, with

electric options becoming more economic

to own and run—even compared to gasoline and diesel engines.[3]

That gap is about to widen more so, with the launch of the SOLO from

veteran Italian carmakers, Intermeccanica, which in 2017 was acquired by

Vancouver-based Electrameccanica

Vehicles Corp. (NASDAQ:SOLO).

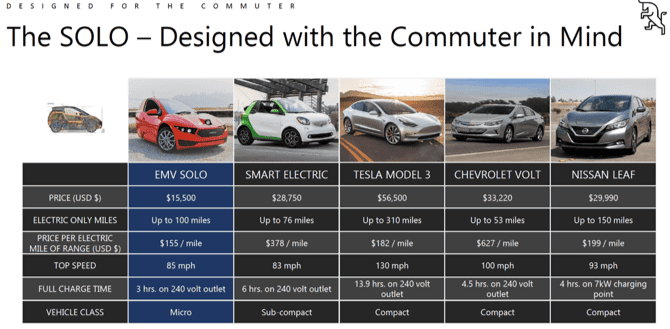

Meet the Market’s Lowest Cost Electric Vehicle

Eye catching

with its unique three-wheeled,

single-seat design,[4]

the game-changing EV currently has another advantage that even the majors can’t

currently touch—its price.

Retailing at ~$15,500 USD, the SOLO is the least expensive EV on the market. Now with a manufacturing agreement with China’s largest motorcycle manufacturer in place, Electrameccanica Vehicles Corp. (NASDAQ:SOLO) is set to further reduce its production risk, and capex, and increase it profit margins.

“Electrameccanica has a total of 64,154 vehicle pre-orders across all models, representing $2.4 billion in potential sales orders”

The company has two other EV’s in various stages of development, including the Tofino, an all-electric two-seat sports car, and the eRoadster, an electric evolution of Intermeccanica’s widely renowned classic vehicle design.

With the SOLO and Tofino, Electra

Meccanica brings a unique, winning EV formula for 2019.

Pre-Orders Galore: Billions in Potential Sales

in Play

As of December 20, 2018, Electrameccanica

Vehicles Corp. (NASDAQ:SOLO) had a total of 64,154 vehicle pre-orders

across all models, representing $2.4 billion in potential sales at the targeted

MSRP.

Pre-orders consist of 23,030

pre-orders for the SOLO single-passenger electric vehicle, which has a

$15,500 target MSRP, and 41,124

pre-orders for the Tofino two-seat roadster sports car, which has a $50,000

target MSRP.

Over a three-year period commencing Q1 2019, Electrameccanica Vehicles Corp. (NASDAQ:SOLO) anticipates the

delivery of 75,000 SOLOs. Capitalizing on an established sales, distribution

and service model, the company will partner with existing dealership networks

to drive sales of the SOLO in non-core markets where the company doesn’t

maintain a dealership presence.

Electrameccanica Vehicles Corp. (NASDAQ:SOLO) will begin its deliveries through existing dealerships in Los Angeles, and Vancouver. So far there has been significant dealer interest worldwide—evidenced by dealer letters of intent for over 21,000 SOLOs.

Electrameccanica Offers First Look From Its China Facility

Learn about the China based Manufacturing facility

Adding Major Industry Experience to Its Board

Electrameccanica has begun adding strategic members to its board to strengthen its automotive industry experience. Most recently, the company appointed Peter Savagian as an Independent Director.

Mr. Savagian is a pioneer in automotive electrification, with a broad expertise in the technology, development, launch and production of electric vehicles. In 1990 he began work on the General Motors EV1, the first modern electric vehicle and was named Chief Engineer of Electric Propulsion Systems in 1998. Later, as General Director of Electrified Propulsion, he built and led multiple teams to innovate, engineer and execute the full range of electrified vehicle propulsion systems. His accomplishments at General Motors include 13 electrified autos brought to production. Notably, these include the first modern Electric Vehicle, the GM EV1, the first plug-in hybrid, the Chevy Volt, and the industry’s first long-range value EV, the Chevy Bolt.

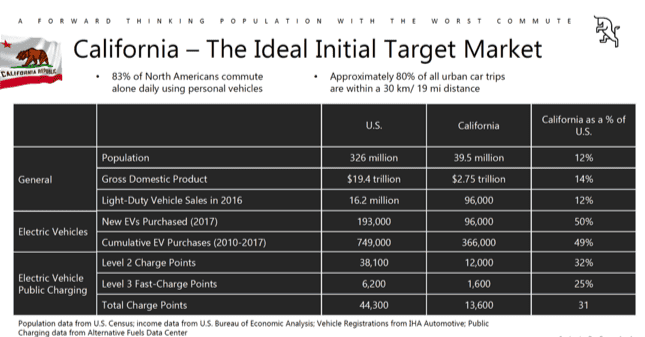

Strong Macroeconomic Markers for the EV Market

As the world begins to make the steady shift into the EV market, some

jurisdictions are more eager than others.

There’s likely no market more eager to get rolling than the state of

California. As the nation’s largest EV market, the Golden State has recently

considered nearly doubling its subsidy for each pure electric vehicle sold in

the state—moving up to $4,500 from $2,500. This is on top of the federal

government’s currently offered $7,500 tax credit on each electric vehicle sold.[5]

Given this environment, Electrameccanica

Vehicles Corp. (NASDAQ:SOLO) has targeted California as the ideal Initial

Target Market.

California is a trend-setter market, with a predilection towards

adopting new technologies and adhering to increasingly progressive policies. With

its extremely high cost of commuting, California has a state-wide goal for EV

adoption, supported by subsidies and investment in charging infrastructure.

With its $15,500 USD price tag, a buyer in California could possibly

see up to $12,000 USD in tax incentives already taken care of for the SOLO—an

overall out-of-pocket discount of more than 77%.

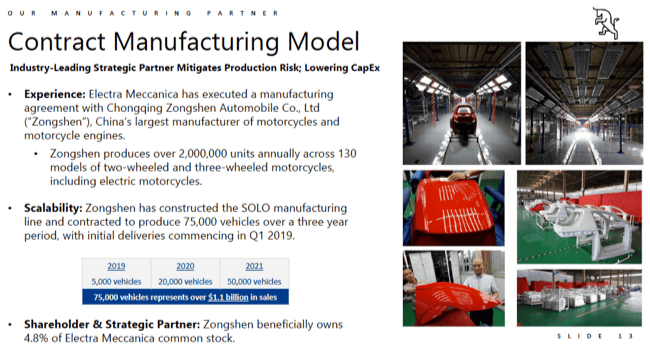

Manufacturing a Chinese EV Advantage

In order to scale production to achieve a strong margin profile,

automakers seeking an advantage in the EV market are looking for a Chinese

manufacturing advantage. Even industry leader Tesla Motors is becoming forthright in its need for China, the

world’s largest auto market, in order to succeed.

Not only is Chinese customer demand and government support for EVs

skyrocketing, but the economic advantage of producing in the country is major.

Tesla CEO Elon Musk has expressed his concern that without

manufacturing in China, Tesla won’t be able to produce the company’s goal of

10,000 Model 3 electric sedans per week nor be able to offer the eagerly

awaited base model at a price of $35,000.[6]

“Bottom line is we need the Shanghai factory to achieve

that,” said Musk.

There’s been a lot of interest for EV makers surrounding China. Volkswagen’s and GM’s SAIC Motor, Warren Buffett-backed BYD, and the recently public NIO are a few among the companies that are already up and running in the country.

For Electrameccanica Vehicles

Corp. (NASDAQ:SOLO), a deal with shareholder and strategic partners,

Chongqing Zongshen Automobile Co., Ltd, has set the SOLO manufacturing line in

motion.

Zongshen is China’s largest manufacturer of motorcycles and motorcycle

engines. The company already produces over 2 million units annually, across 130

models of two-wheeled and three-wheeled motorcycles, including electric models.

Together, the Electra Meccanica

and Zongshen agreement should yield a level of scalability that would deliver a

massive manufacturing advantage for SOLO and the other models. Zongshen has

already constructed the SOLO manufacturing line, and has been contracted to

produce 75,000 vehicles over a three-year period, with initial deliveries

commencing in Q1 2019.

The economic advantage of this arrangement is quite clear, with scaled

gross margins expected in the ~25% range.

This industry-leading contract with a manufacturing partner reduces

production risk for Electrameccanica

Vehicles Corp. (NASDAQ:SOLO), while accelerating production, and notably

minimizes capital expenditures.

MAJOR EV-AUTOMAKER COMPARABLES

So far, the majors in the EV space are working diligently to secure

production for their upcoming lines of vehicles. Each has a unique struggle in

the lead-up to the eventual EV revolution, including getting costs down, making

profitable lines, and securing materials

With a simple line of two offerings, and more to come in the future, Electrameccanica Vehicles Corp.

(NASDAQ:SOLO) has already hit the ground running with the lowest cost EV on

the market.

Here are a few of the ongoing stories in the EV space happening right

now:

The Nevada-based Tesla Motors gigafactory

made headlines over the last few years, as the premiere EV brand name became an

American success story. However, the company has recently made clear its

intentions to enter the Chinese market, and attempt to compete with foreign and

Chinese automakers that are already manufacturing and selling EVs in the

country. CEO Elon Musk admits his company won’t be able to produce 10,000 Model

3 electric sedans per week, as originally aimed. Ahead of Musk’s company, Electra Meccanica has ramped up

production at a new Zongshen factory, for both its SOLO and Tofino models.

—

Kandi Technologies (NASDAQ:KNDI)

Market Cap: $276.77 Million

Kandi Technologies Group, Inc., through its subsidiaries, designs, develops, manufactures, and commercializes electric vehicle (EV) products and parts and off-road vehicles in the People’s Republic of China and internationally. It offers off-road vehicles, including go-karts, all-terrain vehicles, utility vehicles, and other vehicles for sale to distributors or consumers; and EV parts comprising battery packs, EV drive motors, EV controllers, air conditioners, and other electric products.

—

NIO Inc. (NYSE:NIO)

Market Cap: $1.461 billion

NIO Inc. designs, manufactures, and sells electric vehicles in the People’s Republic of China, Hong Kong, the United States, the United Kingdom, and Germany. The company offers five, six, and seven-seater electric SUVs. It is also involved in the provision of energy and service packages to its users; marketing, design, and technology development activities; manufacture of e-powertrains, battery packs, and components; and sales and after sales management activities.

The largest US automaker, General Motors,is

committed to eventually make its entire vehicle lineup “all-electric,” but

doesn’t expect to make them profitably until “early next decade”. While pouring

money into EV technology, looking to capture a market that’s garnered much

excitement thanks to Tesla, General Motors has made it clear that

the company is committed to an all-electric future, with its luxury brand

Cadillac being the lead brand for its electrification efforts. While such

changes are cumbersome for massive automakers, groups like Electra Meccanica are able to capture the early market advantage

with pre-orders and an early run at scalability. As of October, 2018, Electra Meccanica has booked pre-orders

in excess of CAD $2.4 billion and is growing.

—

Strong Leadership Team At The Cutting Edge Of

The EV Space

“I am very pleased with our team’s progress to date. Having

driven the 2019 SOLO myself, I’m convinced we have a winning car on our hands.”

– Electra Meccanica Founder and President,

Henry Reisner

On the road to achieving its goals, Electrameccanica Vehicles Corp. (NASDAQ:SOLO) has been steered by

an experienced leadership team. In order to navigate the rollout of both the

SOLO and the Tofino to a customer base that’s hungry for a new experience

behind the wheel, the Electra Meccanica team

has been crucial to the brand’s successes.

CEO

Paul Rivera joined Electra Meccanica as Chief Executive Officer in August 2019. Before joining Electra Meccanica, Rivera most recently served as President of Ricardo, USA, a division of Ricardo, PLC (LON: RCDO), a 100-year-old global engineering, strategic, and environmental consultancy business with a value chain that includes the design, engineering, testing, and product launch, of vehicle systems, as well as the niche manufacture of high performance products. Previous to that, as Executive VP of Hybrid & Electric Systems at Ricardo, Rivera led the company’s evolution towards an efficient and sustainable low carbon future. Ricardo’s engineering and design solutions have had a significant impact on technical developments throughout the auto sector, providing innovative solutions across engines, drivelines and hybrid systems, as well as supporting the development of emerging technologies such as autonomous and connected vehicles.

Founder

Henry Reisner has served as the President of Intermeccanica since

2001. Intermeccanica is an Italian automobile manufacturer in operation for

over 60 years, which Electrameccanica acquired in 2017. Reisner’s background

includes extensive experience in the automotive industry with a background in

manufacturing. Having overseen early production of the SOLO, he’s expressed his

confidence in the company achieving its goals.

Chief Administrative Officer

With the international aspirations and multinational production and sales goals for the company, Rivera and Reisner are joined by Chief Administrative Officer Isaac Moss. With over 27 years of international business, multi-jurisdictional investment banking and corporate finance experience, Moss’ expertise has ranged across several industries, including specialty chemicals, tech and green energy.

The management team is rounded out by CFO Bal Bhullar, and General

Manager Ed Theobald. Bhullar is an accomplished financial executive with over

25 years of experience, that includes CFO experience at several public and

private companies. Theobald has over 40 years of experience across several

industries, including 19 years as General Manager at Envirotest Canada, a

subsidiary of ESP Global.

1.Lowest-Cost EV on the Market: In this

new era of electric vehicles, to hold the distinction of the lowest cost EV on

the market is a significant advantage for Electrameccanica

Vehicles Corp. (NASDAQ:SOLO). Where the next lowest cost EV at the moment

is the Smart Electric, which is nearly double the price at $28,750, the EMV

SOLO stands in an economic class of its own at an MSRP of $15,500 USD.

2. Over 64,000 Pre-Orders, Worth Billions in

Value: As of December 20, 2018, Electrameccanica

Vehicles Corp. (NASDAQ:SOLO) has accrued a total of 64,154 vehicle pre-orders across all models, representing $2.4 billion in potential sales at the

targeted MSRP. With delivery commencing in Q1 2019, the company will begin

with deliveries through existing dealerships in Los Angeles, and Vancouver—with

significant dealer interest worldwide, evidenced by dealer letters of intent for over 21,000 SOLOs.

3. Strong Macroeconomic Markers for EV Market: