Asian Shares Are Mostly Lower, With Most World Markets Closed for Christmas

Shares are lower in Tokyo and Shanghai, two of only a handful of world markets open on Christmas day

Shares are lower in Tokyo and Shanghai, two of only a handful of world markets open on Christmas day

American consumers are feeling less confident in December, a business research group says

A powerful government panel has failed to reach consensus on the possible national security risks of a nearly $15 billion proposed deal for Nippon Steel of Japan to purchase U.S. Steel

American Airlines briefly grounded flights nationwide due to a technical problem just as the Christmas travel season kicked into overdrive and winter weather threatened more potential problems for those planning to fly or drive

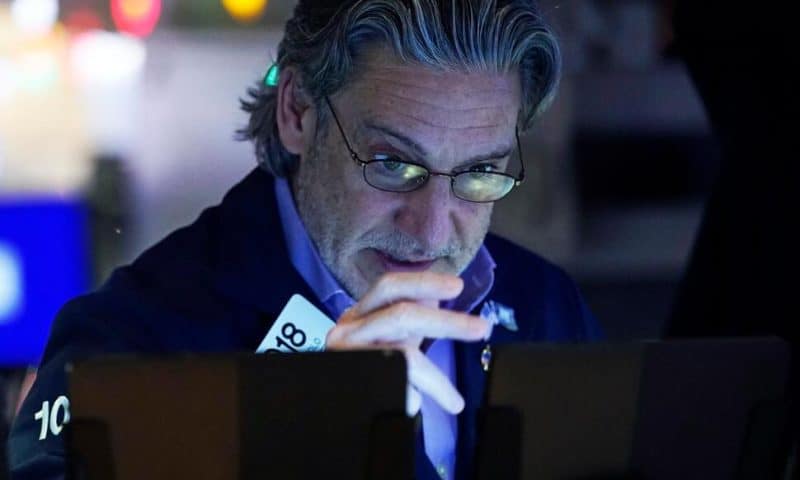

Stocks closed higher on Wall Street ahead of the Christmas holiday, led by gains in Big Tech stocks

Stocks closed higher on Wall Street at the start of a holiday-shortened week

Japanese automakers Nissan and Honda have announced plans to work toward a merger that would catapult them to a top position in an industry in the midst of tectonic shifts as it transitions away from its reliance on fossil fuels

A federal regulator has sued JPMorgan Chase, Wells Fargo and Bank of America

An inflation gauge that is closely watched by the Federal Reserve barely rose last month in a sign that price pressures cooled after two months of sharp gains

U.S. stocks rose to turn what would have been one of the market’s worst weeks of the year into just a pretty bad one

Louisiana, Missouri and Virginia report first measles cases of 2025

Louisiana, Missouri and Virginia report first measles cases of 2025 Using Tech as You Get Older Could Reduce Your Risk of Dementia

Using Tech as You Get Older Could Reduce Your Risk of Dementia Growth across fields: Scientific collaboration tackles farming challenges

Growth across fields: Scientific collaboration tackles farming challenges New possibilities for animal-computer interaction to benefit zoo animals and visitors

New possibilities for animal-computer interaction to benefit zoo animals and visitors UT Health San Antonio scientists pioneer drug-discovery breakthrough for large and polar drugs

UT Health San Antonio scientists pioneer drug-discovery breakthrough for large and polar drugs StockWatch: Investors Hungry for Lilly after Diabetes Pill Aces Phase III Trial

StockWatch: Investors Hungry for Lilly after Diabetes Pill Aces Phase III Trial New antibiotic is effective against gonorrhea, could be first new treatment since 1990s, study says

New antibiotic is effective against gonorrhea, could be first new treatment since 1990s, study says What are SSRIs? Explaining the antidepressant medication

What are SSRIs? Explaining the antidepressant medication ‘Magic carpet’ guides cells to self-organize in 3D

‘Magic carpet’ guides cells to self-organize in 3D WuXi Biologics Reports Completion of First Commercial PPQ Campaign at 15,000 L Production Line

WuXi Biologics Reports Completion of First Commercial PPQ Campaign at 15,000 L Production Line