The Bank of England has repeated its previous policy of holding rates, mirroring precisely the Monetary Policy Committee’s May 9 vote on UK interest rates.

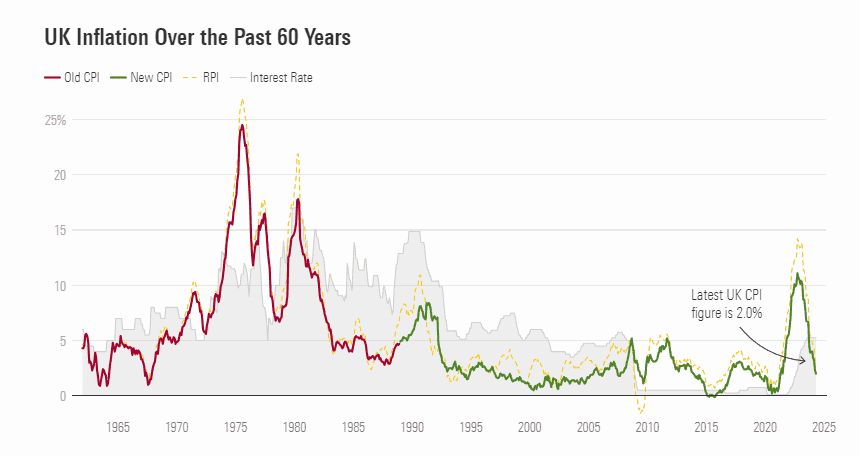

A majority of 7-2 once more opted to hold rates, in defiance of what some felt was a pressure to lower rates now that inflation has hit the Bank’s own 2% target.

The decision means the Bank of England’s base rate will stay at 5.25%, a level it has been held at since August 2023. A cut is now seen as most likely to occur in August 2024, according to financial markets, when the monetary policy report is published and the Bank holds its press conference.

Today’s decision was widely expected so the stock, bond and currency market response was muted.

Why Has The BoE Held Rates?

In a statement, the BoE said a return to the 2% target had not been enough to convince the MPC to vote wholeheartedly for a cut.

“For some members within this group, the return of headline inflation to 2%, while welcome, was not necessarily indicative of the required sustained return to target,” it said.

“Continued high levels of, and upside news to, services inflation supported the view that second-round effects would maintain persistent upward pressure on underlying inflation.

“Wage growth had continued to exceed model-based estimates. Indicators of domestic demand were stronger than had been expected, and the risks to the outlook for activity were skewed to the upside.

“For these members, more evidence of diminishing inflation persistence was needed before reducing the degree of monetary policy restrictiveness.”

The statement will indicate to investors and traders that the BoE is approaching a rate cut very cautiously indeed, and that it could be some time before rates come down.

This is something of a departure from the upbeat picture markets had expected at the end of last year, when it was thought 2024 would be see multiple cuts by the world’s central banks. In the US, some expected as many as five rate cuts in 2024.

Rate Cuts – They’re Coming

Commenting on the news, Michael Field, Morningstar’s European market strategist, says rate cuts are now a question of when not if.

“The MPC’s previous [May] statement contained a number of caveats, particularly around services inflation. We see this less so in today’s statement, with an overall acknowledgement that inflation has fallen sufficiently, as headline inflation for the UK in May fell to 2%, in line with the Bank’s targeted level,” he says.

“We expected that the vote split among committee members might have changed from the 7-2 level last month, but this was not the case. We are not dismayed by this, however, as the MPC often moves as a pack.

“Some investors will naturally be disappointed not to see an early rate cut, but if there’s one important takeaway from today’s statement, it is that the MPC is following the data. The data is clearly moving in the right direction, and therefore, rate cuts will have to follow.”

How Are Fund Managers Reacting to the Rate Hold?

In a note, Georgina Hamilton, fund manager of the Morningstar 4 Star and Gold-Rated Polar Capital UK Value Opportunities Fund, says the BoE is now clearly pursuing a “no surprises” approach.

“Core inflation should [now] start to show progress, paving the way for the BoE to clearly signal to the market their next move is to cut, likely in August,” she says.

“Today’s move certainly signals one thing: the BoE wants no surprises when it actually does cut. It will want sterling to remain calm over the rate cuts, but will no doubt take comfort from the foreign exchange market’s reaction to other central banks cutting rates.

“From our own conversations with housebuilders and consumer-exposed stocks, we know many consumers are waiting for an actual move in rates before making bigger spending decisions.

“While there has been a great deal of focus on the BoE cutting rates ahead of the Federal Reserve – which is unusual – we feel the more interesting debate is where UK interest rates end up. Currently, the market is pricing UK rates to fall to 3.5%, similar to the US rate curve; interestingly, the Eurozone is over 1% lower at 2.4%.”

How Would a Future Interest Rate Cut Affect Me?

As the Bank announces another rate hold, chatter turns to when the cutting cycle might begin. But what would that mean for consumers, and, crucially, those with savings and investments?

As interest rates decrease, cash savings rates on bank accounts and ISAs will likely decrease, meaning savers may start getting less bang for their buck at the bank.

However, lower rates will also make consumer debt cheaper, which could bring relief to people with substantial credit card debt – and mortgage holders with variable-rate products. Those who have remortgaged into fixed-rate products in the last two years may not feel this until they remortgage once more.

What Will Equities and Bonds do if Rates Are Cut?

Markets tend to “price in” any changes very quickly, so the reaction to this kind of news will be swift. Conventional wisdom suggests rate cuts are better for equities than bonds. But while bonds have returned to favour in the higher interest rate era because of their tempting yields, rate cuts may not be bad for them either.

Falling interest rates mean lower yields, which push bond prices ever higher – a key factor in total returns. And lower rates make existing bonds, and particularly those already issued during a period of rate hikes, more attractive for yield.

In addition, many pension funds, for whom rising bond yields have caused havoc, could also stand to benefit from a looser monetary approach. This may well benefit the government’s attempts to reignite the UK’s stagnant economy as (in theory) it encourages institutional investors to plough money into promising growth businesses.

How Will The Real Economy React?

Over in the “real economy”, the unwinding of monetary policy will likely also benefit shops and online businesses who have been squeezed by the twin spectres of supply chain inflation and lower consumer confidence. If higher interest rates have the power to curb spending in the UK economy and cool gross domestic product growth, lower rates will in theory create the opposite effect.

In practice, however, there is a lot of uncertainty. While lower interest rates tend to stimulate the economy, the UK is still expected to suffer from low growth in the coming years wherever rates end up. Either way, it will take time for the precise effects to be visible, let alone quantifiable.