Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that ABL Bio Inc. (KOSDAQ:298380) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

What Is ABL Bio’s Debt?

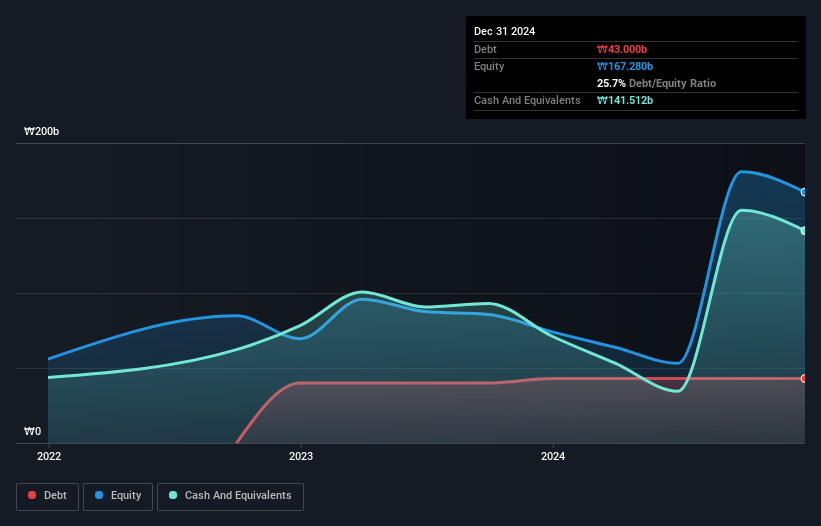

The chart below, which you can click on for greater detail, shows that ABL Bio had ₩43.0b in debt in December 2024; about the same as the year before. However, it does have ₩141.5b in cash offsetting this, leading to net cash of ₩98.5b.

How Strong Is ABL Bio’s Balance Sheet?

We can see from the most recent balance sheet that ABL Bio had liabilities of ₩63.4b falling due within a year, and liabilities of ₩1.34b due beyond that. Offsetting these obligations, it had cash of ₩141.5b as well as receivables valued at ₩827.2m due within 12 months. So it can boast ₩77.6b more liquid assets than total liabilities.

This surplus suggests that ABL Bio has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, ABL Bio boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if ABL Bio can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year ABL Bio had a loss before interest and tax, and actually shrunk its revenue by 49%, to ₩33b. To be frank that doesn’t bode well.

So How Risky Is ABL Bio?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year ABL Bio had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of ₩78b and booked a ₩56b accounting loss. However, it has net cash of ₩98.5b, so it has a bit of time before it will need more capital. Overall, its balance sheet doesn’t seem overly risky, at the moment, but we’re always cautious until we see the positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we’ve discovered 1 warning sign for ABL Bio that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don’t even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.